2019-09-19

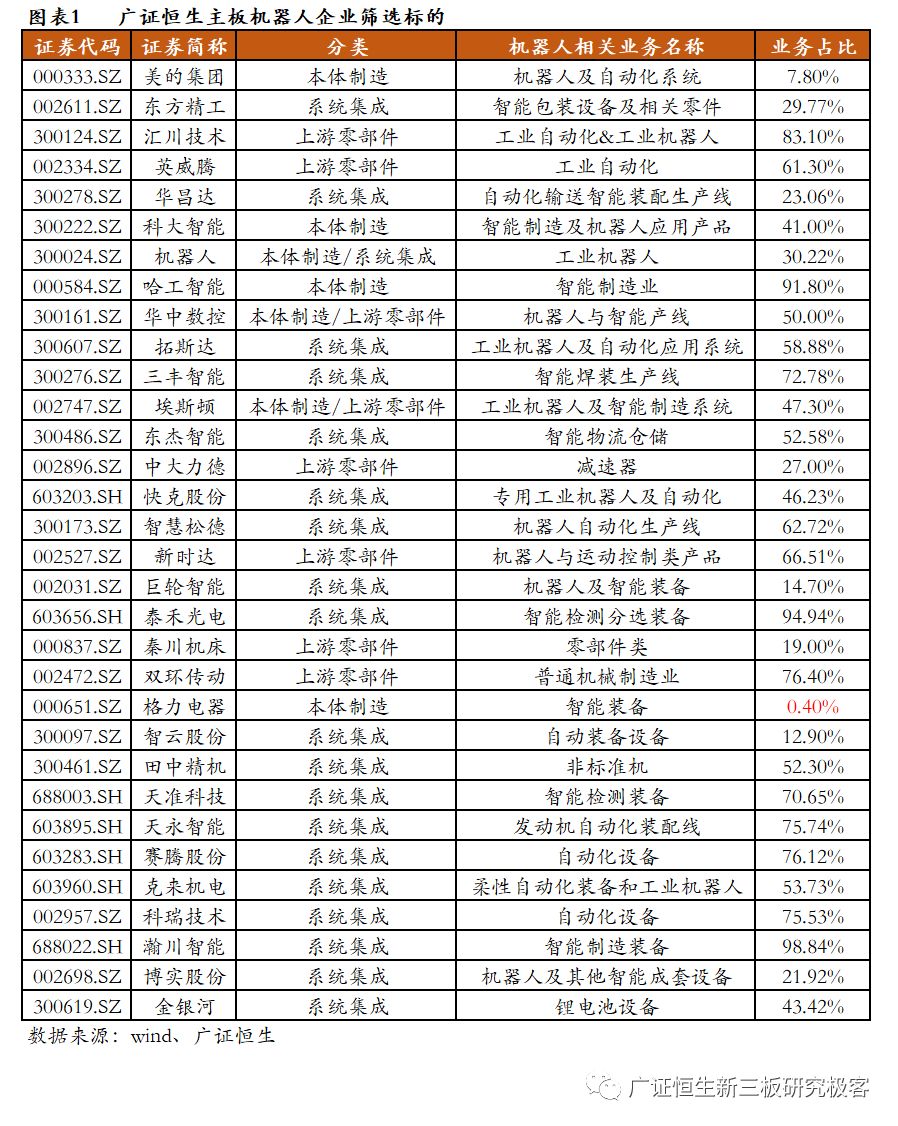

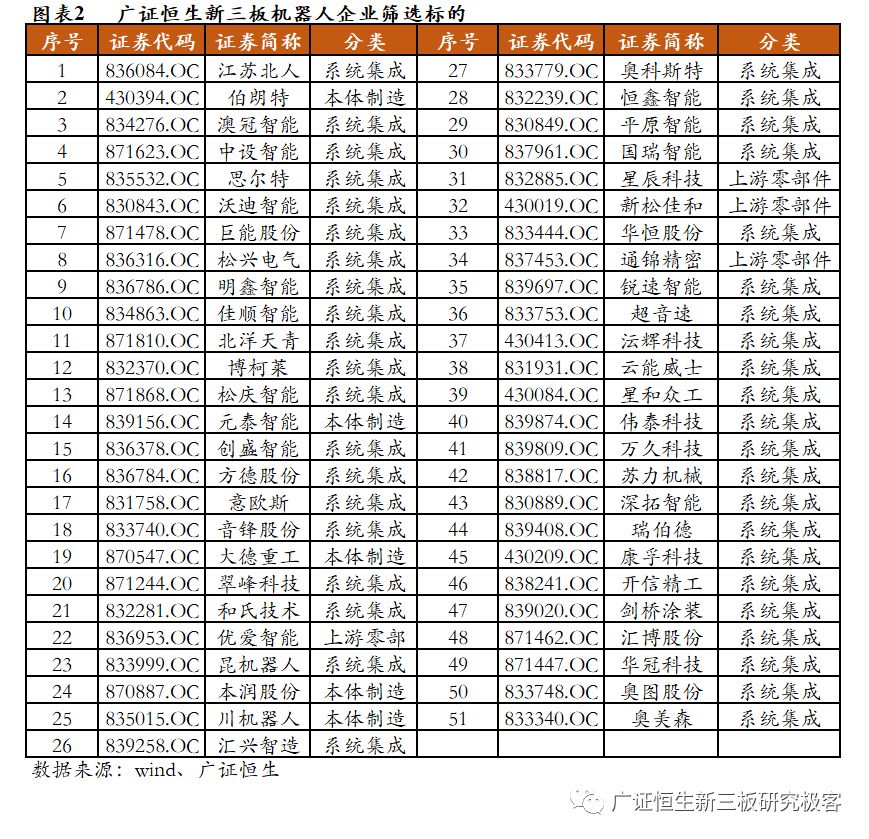

As of September 2019, the 2019 interim report of the main board and new Third Board Companies in the industrial robot market has been basically disclosed. After screening and analyzing the business scope and main business composition of the new third board and main board enterprises, we selected 32 main board enterprises and 51 new third board enterprises as the analysis targets. Because most industrial robot enterprises have a wide range of downstream application fields, which is difficult to be simply classified by automobile and 3C industries, we classify enterprises mainly engaged in downstream application fields as system integration.

In the first part, we will use the main financial data to compare and analyze the financial situation of enterprises from five aspects: operating revenue, operating profit, net profit, R & D investment, and net cash flow from operating activities, divided into three categories: overall situation, new third board and main board enterprises. In the second part, we choose eston, A-share enterprise engaged in ontology manufacturing, and Fanuc, one of the four families, as representative enterprises, to analyze the reasons for the changes in their financial data and confirm the development trend of the industry.

Among the main board enterprises, Midea and Gree have a low proportion of robot business revenue, and there is no corresponding net profit, R & D expenses and other financial information. Therefore, in this paper, in addition to analyzing the revenue, the impact of these two enterprises is considered, and these two enterprises are not considered in other financial data analysis. In addition, due to the lack of some data of last year for recently listed companies such as Tianzhun technology, such companies will be removed from the calculation.

1. Analysis of financial performance of industrial robot industry in the first half of the year

1.1 in the first half of 2019, the operating revenue increased by 0.9% year-on-year

In the first half of 2019, the development speed of the robot industry slowed down. According to the statistical data of high-tech robots, the output of China's industrial robots in the first half of 2019 was 75400, a year-on-year decrease of 10.1%; The sales volume was 78000 units, a year-on-year decrease of 10.8%. Since most of the main board enterprises are engaged in robot business and other businesses at the same time, we only select the operating revenue of the robot business to calculate and analyze; Most of the new third board enterprises are engaged in the application of robots in the downstream field. Because the robot business accounts for a large proportion and some enterprises do not disclose the proportion of sub field business, we directly use the company's operating revenue as the robot business revenue. We selected 83 target enterprises,In the first half of 2019, the total operating revenue reached 29.39 billion, with an average operating revenue of 350 million yuan, an increase of 0.9% year-on-year. Among them, the total operating revenue of main board enterprises was 25.55 billion, an increase of 2.2% year-on-year; The total operating income of enterprises on the new third board was 3.83 billion, a year-on-year decrease of 6.8%.

Although the revenue growth rate of main board enterprises is positive, there is still a certain gap compared with 10.96% in mid-2018. The decline in the growth rate of main board revenue is largely affected by the -3.8% growth rate of Midea Group's robot business revenue. After removing Midea Group, the total revenue growth rate of the other 30 enterprises was 8.1%. In addition, in the first half of 2019, the development of automotive, 3C and other major industries in the downstream field of robots slowed down. Due to the comprehensive impact of the macroeconomic downturn and the high level of automobile sales base, China's total automobile sales volume showed negative growth for the first time in 2018, and the automobile sales volume in the first six months of 2019 was negative growth. At the same time, affected by the slowdown of economic growth and the low-level operation of metal forming machine tools and other industries, the business income of numerical control system decreased slightly compared with the same period, resulting in the year-on-year growth rate of business income of enterprises engaged in numerical control business and robot business at the same time, such as Easton, Qinchuan machine tools, etc., which decreased compared with 2018.

The growth rate of the new third board enterprises' revenue is negative, which is closely related to the slowdown in the development of the robot industry. Some small enterprises have not achieved economies of scale and have no other business support, resulting in a decline in revenue.

Among the 83 target enterprises we selected, 45 enterprises have an operating income of more than 100million yuan, accounting for 54.2%, of which 9 enterprises have a revenue of more than 1billion yuan, all of which are mainboard enterprises. Midea Group, which acquired KUKA, ranked first in terms of revenue. Its robot business revenue exceeded 10 billion in the first half of 2019, but decreased by 3.8% compared with the same period in 2018; The second is Dongfang Seiko in the field of system integration and Huichuan technology in the field of servo motor in the field of upstream parts. In the new third board, the highest operating income is plain intelligence in the downstream system integration field, followed by Huaheng shares and Bronte, who is engaged in ontology manufacturing.

In terms of revenue growth rate, 49 enterprises achieved positive growth, accounting for 59%; The revenue growth rate of 10 enterprises exceeded 50%, of which the revenue of Huaguan technology exceeded 400% (mainly due to the equipment revenue of 49.5017 million yuan in the operating revenue during the reporting period, an increase of 42.5212 million yuan or 609.14% from 6.9805 million yuan in the same period last year). The growth rate of Zhiyun shares with a relatively low growth rate was -66.4% (the main reason is that 3C intelligent manufacturing equipment sector was affected by the overall economic environment, industry transformation cycle, customer structure adjustment, product structure adjustment and other factors, and the growth rate of market demand slowed down; while the emerging product market is still in the stage of expansion, so the order size was reduced, the settlement was delayed, and the company increased R & D investment, resulting in a significant year-on-year decline in revenue and net profit.)

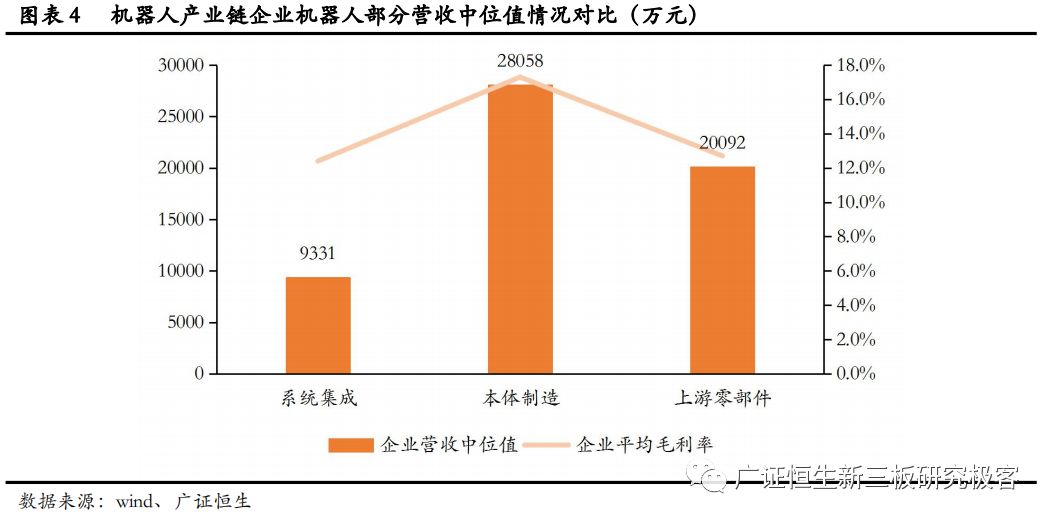

We further classified 83 enterprises according to the different positions of the industrial chain, and analyzed their total operating income. Since the average revenue of enterprises is easily affected by extreme values, we mainly use the median value of enterprise revenue to analyze. It can be found that the highest median value of operating income is 280.58 million yuan for ontology manufacturers, followed by 20.92 million yuan for upstream component manufacturers, and finally 93.31 million yuan for system integrators. In terms of gross profit rate, the average gross profit rate of upstream component manufacturers and system integrators is not much different, both of which are about 12%. The gross profit rate of ontology manufacturing enterprises is the highest, which is 17%, which is about 5 percentage points higher than the average gross profit rate of enterprises in the other two industrial chain fields.

1.2 the average net profit in the first half of 2019 decreased by 39% year-on-year

Compared with 2018, the growth rate of robot enterprises slowed down, and the net profit growth rate was negative. Since the company did not disclose the specific net profit of the robot business, we considered the overall net profit of the company in the first half of 2019 and analyzed the overall situation of 81 enterprises (excluding Midea and Gree). The total net profit of 81 enterprises was 1.53 billion yuan, and the average net profit of each enterprise was 19 million yuan, a year-on-year decrease of 39% compared with the net profit of the same period in 2018. According to the classification of main board enterprises and new third board enterprises, the total net profit of main board enterprises was 1.29 billion yuan, with an average of 43 million yuan, a year-on-year decrease of 42.1% compared with the same period in 2018; The total net profit of enterprises on the new third board was 230million yuan, with an average of 05million yuan per enterprise, a year-on-year decrease of 16.8% compared with the same period in 2018. It can be seen from this that the profitability of the robot industry decreased significantly in the first half of 2019.

Among 81 enterprises, 61 have positive net profits, accounting for 75.3%. Among the 30 enterprises on the main board, 25 have positive net profits, accounting for 83.3%; Among the 51 Enterprises on the new third board, 36 have positive net profits, accounting for 70.6%. Among the 81 enterprises, only 6 have net profits of more than 100million yuan, all of which are mainboard enterprises (Huichuan technology, robotics, Dongfang Seiko, Boshi, Sanfeng intelligent, Kerui Technology). Among them, Huichuan technology in the upstream parts field, with the highest net profits, has a net profit of 430million yuan (but a year-on-year decrease of 15.9% compared with the same period in 2018)

Among the main board enterprises, Huichuan technology has the largest net profit, and huachangda has the smallest (during the reporting period, the accrued estimated liabilities were 279million yuan, the accrued goodwill impairment was 83.3106 million yuan, and the loss on disposal of fixed assets was 46.8407 million yuan); Among the new third board enterprises, the largest net profit is Pingyuan intelligence and the smallest is Yinfeng shares.

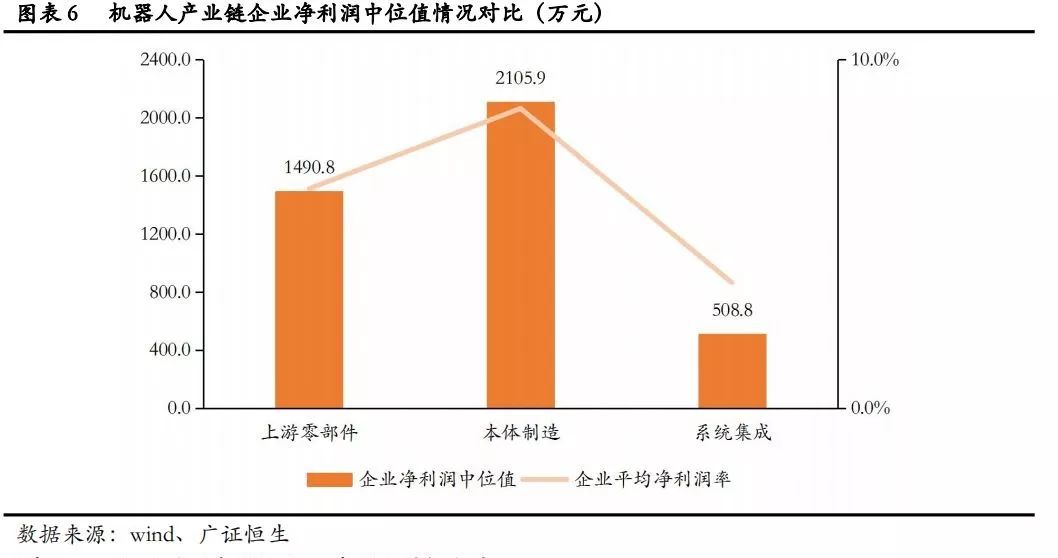

From the perspective of industrial chain and downstream application fields, the median value of enterprise net profit of upstream component manufacturers is 14.908 million yuan, the median value of enterprise net profit of ontology manufacturers is the largest, which is 21.059 million yuan, and the median value of enterprise net profit of system integrators is the smallest, which is 5.088 million yuan.

In terms of net profit margin, the average net profit margin of enterprises in all links of the industrial chain is less than 10%, of which the net profit margin of ontology manufacturers is the highest, 8.6%. The average net profit margins of upstream parts enterprises and system integration enterprises are 6.3% and 3.6% respectively, 2-5 percentage points lower than that of ontology manufacturing enterprises.

1.3 net cash flow from operating activities:The total amount of the main board changed from negative to positive, and the total amount of the new three boards continued to be negative

Due to the lack of data from Tianzhun technology and Hanchuan intelligence, we only analyze the situation of the remaining 28 motherboard robot enterprises. The net cash flow from operating activities of enterprises on the main board totaled 1.44 billion yuan, a positive number from -350 million yuan in the same period last year. The net cash flow from operating activities of enterprises on the new third board totaled -380million yuan, which continued to decline on the basis of -330million yuan in the same period in 2018.

Among the main board enterprises, there are 14 enterprises with positive net cash flow from operating activities, accounting for 50%, Among them, the net cash flow from operating activities of Dongfang Seiko is the largest (affected by the adjustment of subsidy policies, impulse of power battery manufacturers in the transition period and other factors, the sales revenue recognized by the subsidiary Prader in the reporting period increased significantly compared with the same period of last year; at the same time, "high-end intelligent equipment business" The overall revenue of the sector increased steadily in the first half of the year, resulting in a significant increase in the group's consolidated statement level operating income. Affected by the substantial increase in sales revenue, the net cash flow from operating activities also increased significantly in the reporting period); The net cash flow of robot business activities is the smallest. Among the new third board enterprises, the net cash flow from operating activities of 20 enterprises was positive, accounting for 39%.

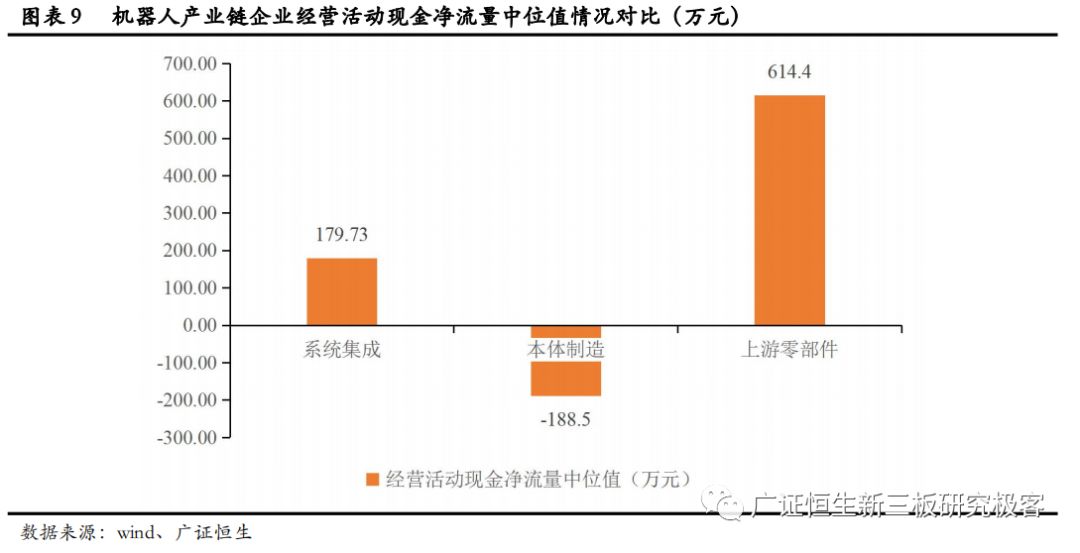

From the perspective of industrial chain and downstream application fields, the median value of net cash flow from operating activities of upstream component manufacturers and system integrators is positive, which is 6.144 million yuan and 1.797 million yuan respectively. The median value of net cash flow from operating activities of ontology manufacturers is negative, -1.885 million yuan.

1.4 R & D expenses increased by 12.4% year on year

Since Juneng Co., Ltd., a new third board enterprise, did not disclose the information of R & D expenses, we only analyzed 80 enterprises. In the first half of 2019, the total R & D investment of enterprises was 2.01 billion yuan, an increase of 11.4% year-on-year compared with 1.82 billion yuan in the first half of 2018, and the average R & D investment of each enterprise was 25 million yuan. Among them, the R & D investment of main board enterprises totaled 1.77 billion yuan, with an average R & D cost of 59 million yuan, an increase of 12.4% year-on-year; The total R & D investment of enterprises on the new third board was 260million yuan, with an average R & D cost of 5.15 million yuan, an increase of 4.9% year-on-year. It can be found that the growth rate of R & D investment of mainboard enterprises is large, and the average R & D investment is also large. However, although the overall R & D expenses of enterprises increased by more than 10%, there is still a certain gap from the growth rate of 27.2% in 2018.

In terms of growth rate, 57 of the 81 enterprises increased their R & D investment in the first half of 2019, accounting for 70.4%, of which 8 enterprises increased their R & D investment by more than 100%. The top three main board enterprises in terms of year-on-year growth rate are Huichuan technology, yingweiteng and Kerui technology, and the new third board enterprises are Huaheng Co., Ltd., Pingyuan intelligence and Bronte.

As robots are intelligence intensive and high value-added industries, we should focus on enterprises with large R & D costs and high revenue. For 80 enterprises, the proportion of R & D investment in revenue increased from 4.7% in the first half of 2018 to 5% in the first half of 2019, an increase of 0.3 percentage points. The proportion of R & D investment in revenue of main board enterprises also increased by 0.3 percentage points; The proportion of R & D investment in revenue of enterprises on the new third board increased by about 0.75 percentage points. Among the top ten enterprises in R & D cost rate, only one enterprise is a motherboard enterprise (Central China CNC).

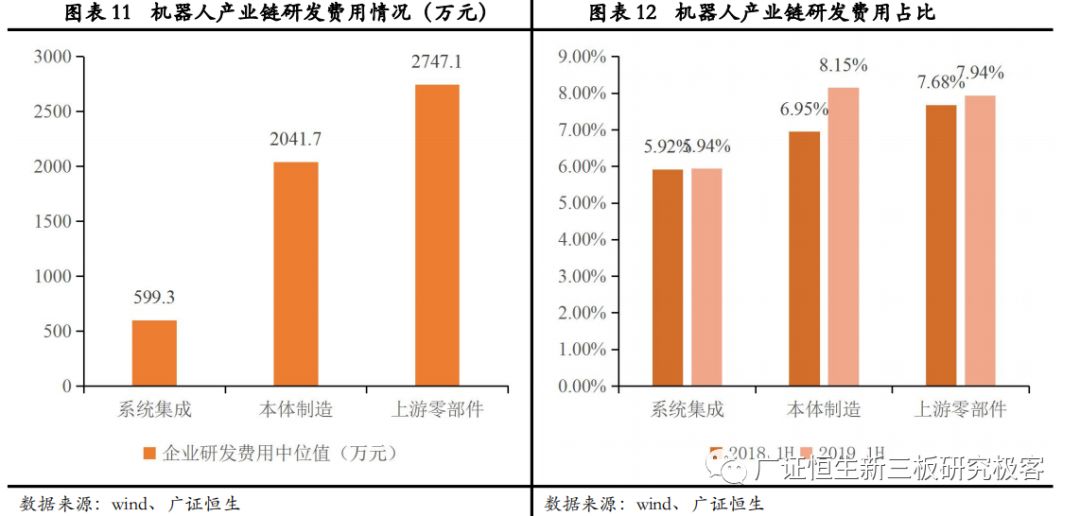

From the perspective of industrial chain and downstream application fields, the proportion of R & D expenses of system integrators, ontology manufacturers and upstream component manufacturers has gradually increased. The overall R & D expenditure accounted for 6.92%, and the R & D expenditure of system integrators did not reach the average. However, in the ontology manufacturing and upstream parts manufacturing fields with high technical requirements, their R & D investment accounted for a high proportion of revenue, 8.15% and 7.94% respectively. In addition, the net value of R & D expenses of upstream parts manufacturers is also large, and the median value of enterprise R & D expenses can reach 27.471 million yuan.

2 Analysis of robot representative enterprises

2.1 esten (002747.sz):Endogenous extension to create industry leader

Nanjing Easton Automation Co., Ltd. was founded in 1993. At the initial stage of its establishment, its main product was the numerical control system of metal forming machine tools. After years of development, the company has not only become one of the leading enterprises in the core control functional components of high-end intelligent equipment in China, but also has entered the industrial robot industry on the basis of its core component advantages, and has become the main force enterprise of domestic robots with independent technology and core components.

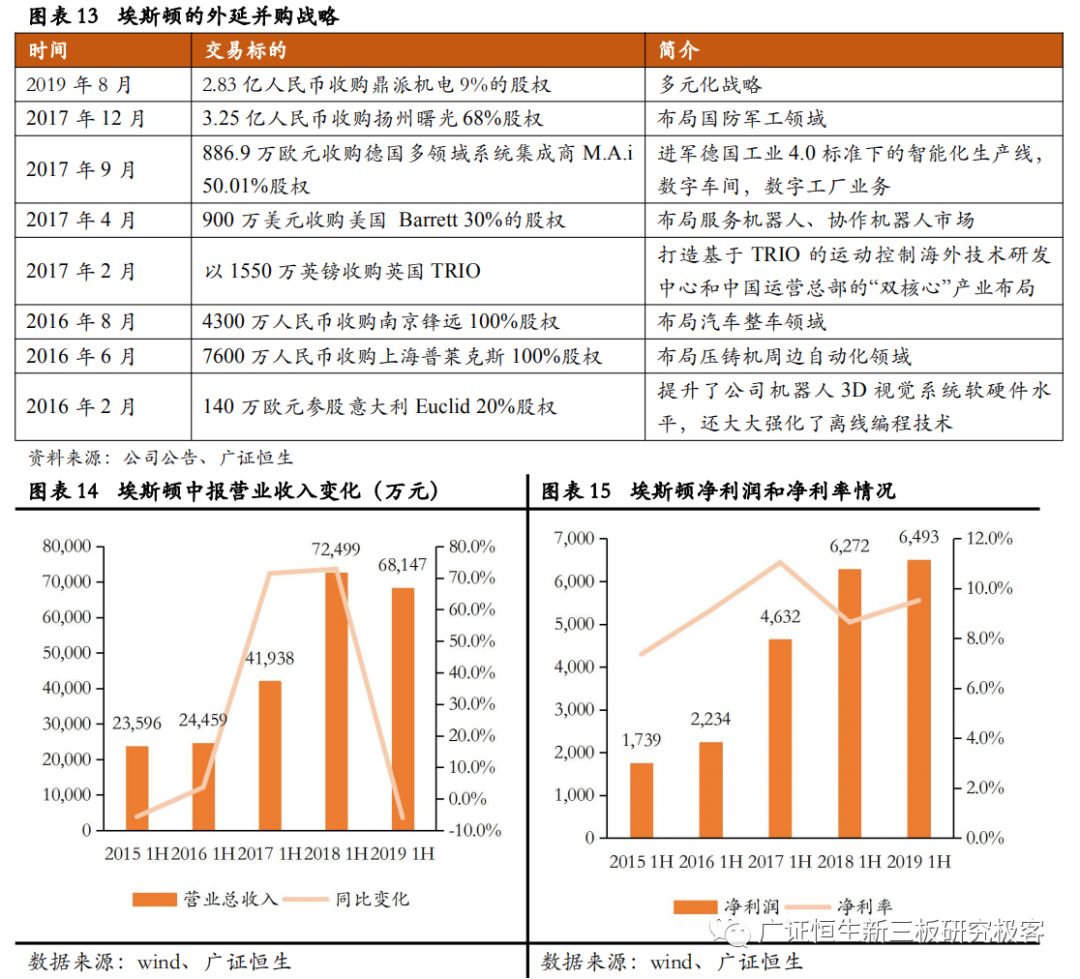

The company has the competitive advantage of the whole industry chain. Its business covers the whole industry chain from automation core components and motion control systems, industrial robots to intelligent manufacturing systems with robot integrated applications. It has built a comprehensive competitive advantage from technology, cost to service, and achieved cost reduction through volume production. As a private enterprise leader in the domestic robot industry, the company has continued to make efforts in the field of industrial robots since 2016. We actively expanded our business through extensive mergers and acquisitions, and successively acquired Shanghai plex, Yangzhou Shuguang, American Barrett technology, British motion controller trio, Dingpai technology and other companies. At present, the whole industrial chain layout of "core parts ontology system integration" has been realized.

From 2015 to 2018, with the vigorous development of the robot industry and the continuous improvement of the company's brand image, eston's operating revenue increased rapidly, reaching a growth rate of more than 70% in the middle of 2017 / 2018. In the middle of 2019, due to the insufficient demand of the industrial control market, especially in the downstream markets of traditional industrial control applications, such as textile machinery, 3C and other original advantageous industries, the robot industry entered a stage of slowdown, and the revenue of the company's two main business segments (Automation core components and motion control systems, industrial robots and Intelligent Manufacturing Systems) fell year-on-year. However, due to the company's active development of advanced technology to reduce product costs and improve management efficiency, the net interest rate of the company in the middle of 2019 increased compared with 2018.

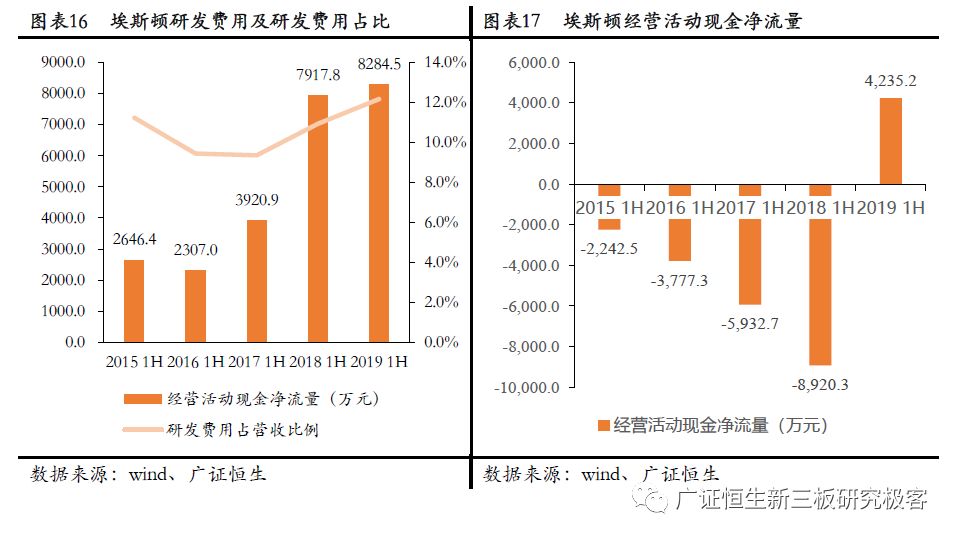

The R & D expenses and the proportion of R & D expenses in operating revenue of Aston have increased year by year since 2017. The company pays attention to technology research and development and has made some breakthroughs. As of June 30, 2019, the company has 309 authorized patents, including 104 invention patents and 166 software copyrights. 121 patents have been applied for but not yet authorized. In the first half of 2019, the R & D investment was 82.8446 million yuan, accounting for 12.16% of the revenue.

The net cash flow from operating activities of Easton continued to be negative in the middle of 2015-2018 and decreased year by year. However, in the first half of 2019, the company carefully selected industries and customers, strictly controlled accounts receivable and increased collection efforts. At the same time, in the macro environment where the economic situation shows no obvious signs of recovery, we set up a risk prevention and control line and actively give up some projects with poor payment collection conditions, making the net cash flow of operating activities from negative to positive.

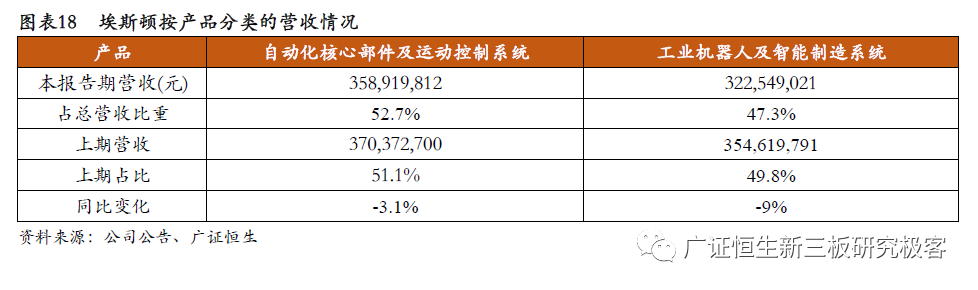

It can be seen from the revenue of esten's sub products that the revenue of both parts has decreased, which is mainly due to the low operation with the automotive and metal machine tool industries, resulting in a year-on-year decline in the business income of intelligent equipment manufacturing and CNC systems. There is no significant change in the proportion of revenue of the two different types of products, and the proportion of revenue is close to 1:1.

1) During the reporting period, the demand of industrial control market was insufficient, and the original advantageous enterprises in the downstream markets of traditional industrial control applications, such as textile machinery and 3C, declined significantly. At the same time, the business was facing the pressure of price reduction of foreign servo brands. The company took advantage of the transformation opportunity to seize the growth opportunities of new industries such as lithium batteries and photovoltaic equipment, and obtained batch orders from key customers based on the trio motion control complete solution. In the first half of 2019, the revenue of motion control and AC servo business increased year-on-year, and the share of complete motion control solutions was quickly listed, reaching 51.69%.

2) Affected by the slowdown of economic growth and the low-level operation of metal forming machine tools, the business income of CNC system decreased year-on-year.

3) Due to the continuous improvement of the performance and technology of industrial robots, the company's industrial robot business has maintained a high rate of growth in the less economic market environment, and is at the industry advanced level in the fields of machine tool loading and unloading, tram welding and so on.

4) Due to the weakening downstream demand, in order to prevent the substantial occupation of funds and prevent the risk of capital chain, the company abandoned some intelligent manufacturing system projects in the automotive industry with poor payment collection conditions, because the business income of intelligent manufacturing system decreased by about 20% year-on-year.

2.2 FANUC (6954. T):One of the four families of robots

Fanuc, founded in 1956, is a Japanese company specializing in numerical control systems. It is the largest professional CNC system manufacturer in the world, accounting for 70% of the global market share. Since the first robot of FANUC came out in 1974, FANUC has been committed to leading and innovation in robot technology. At present, there are 240 kinds of FANUC robot product series. The company operates three business departments: FA department is engaged in the development, manufacturing, sales and maintenance of FA products, such as computer digital control (CNC) systems and laser products. The robot department is engaged in the development, manufacturing, sales and maintenance of robot products. The robotics department develops, manufactures, sells and maintains robodrill, roboshot, robocut and robonano products.

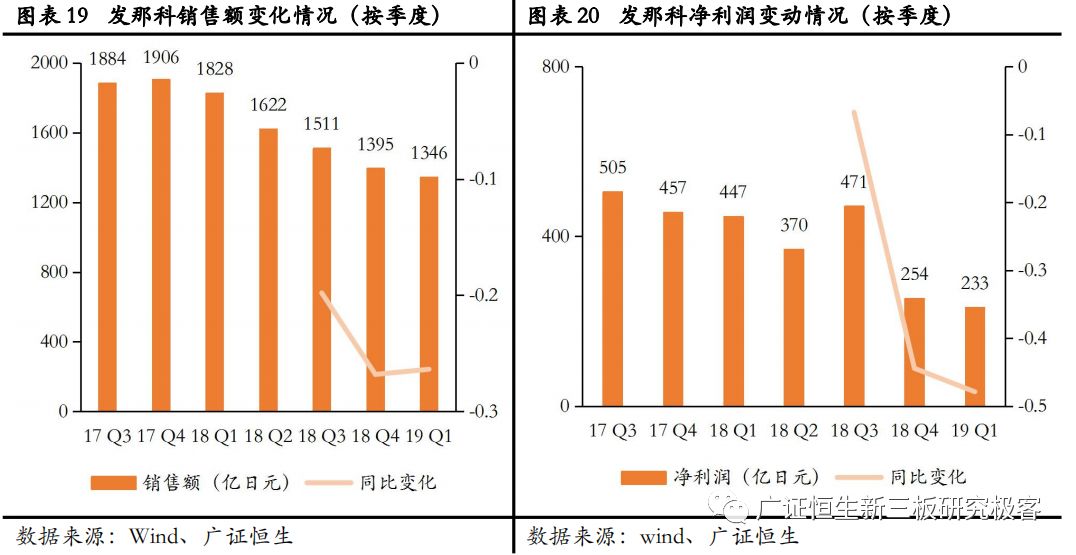

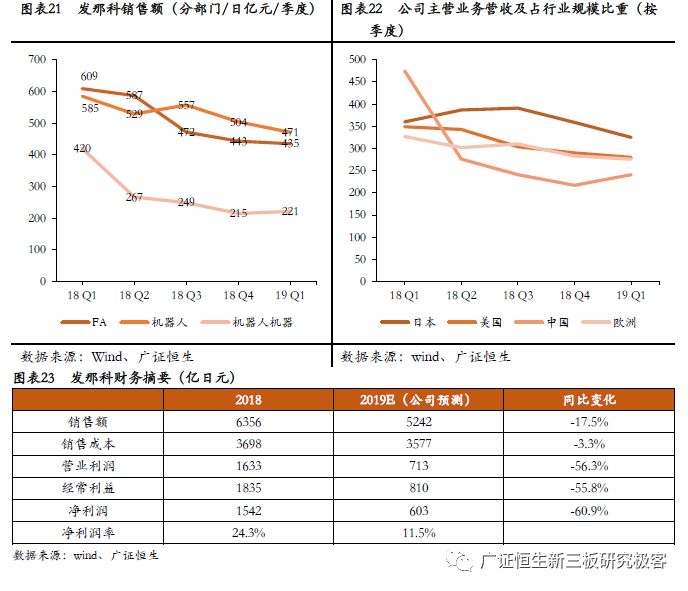

Fanuc's sales have continued to decline since the fourth quarter of 2017, from 190.6 billion yuan in the fourth quarter of 2017 to 134.6 billion yen in the first quarter of 2019. In the first quarter of 2019, the year-on-year growth rate was -26.4%. Meanwhile, the net profit has also continued to decline since the third quarter of 2018. The net profit in the first quarter of 2019 was only 23.3 billion yen, a year-on-year decrease of -44.4%. Fanuc achieved negative year-on-year growth in sales and net profit for three consecutive quarters.

We analyze the main factors of FANUC's sales and net profit changes, and we can find that the sales of the three main businesses have declined, of which the sales of FA (automatic control) have declined the fastest. At the same time, looking at the sales of products by region, we can see that although the global robot industry is in the stage of slowdown, there is no significant decline in sales in Japan, the United States and Europe. In China, due to the slowdown in the development of the real economy, the downward trend in the development of robot downstream automotive and 3C fields and other reasons, FANUC experienced significant sales changes between the first quarter and the second quarter of 2018. According to the current development trend, FANUC has also given its performance forecast for the whole year of 2019, as shown in the table below.

0755-89480969

info@powercome.hk

B1202, building 1, Mogen Fashion Industrial Park, No. 10, shilongzi Road, Xinshi community, Dalang street, Longhua District, Shenzhen

www.powercome.hk