2020-11-25

1. Talk every Monday: the improvement of downstream demand leads to the rebound of lithium iron phosphate price

1.1 the demand for lithium iron phosphate in many fields increased significantly

In the past few years, the growth of lithium iron phosphate shipments has been mainly applied in the field of new energy passenger cars and special vehicles. With the increasing pressure of cost reduction of new energy vehicles and passenger cars and the rapid development of renewable energy power generationEnergy storageWith the increase of demand and the accelerated iteration of 5g base stations,New energy passenger vehicles, energy storage and 5g base stations will become new demand growth points for lithium iron phosphate in the future。

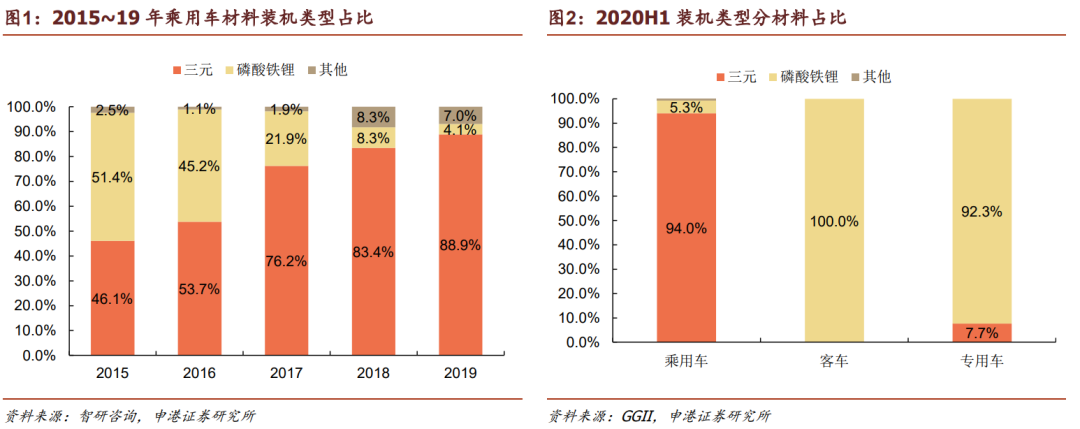

As the new energy vehicle industry enters the "post subsidy era" in which subsidies gradually decline, the cost advantage of lithium iron phosphate has been paid attention to by the passenger car market again.From 2015 to 19, the new energy vehicle market developed rapidly,Ternary lithium batteryThe energy density is dominant, the market share is gradually increasing, and it occupies the mainstream position of the passenger car market. At the same time, lithium iron phosphate has shrunk significantly in the passenger car market. With its cost advantage, it is mainly used in the passenger car and special vehicle market. In the passenger car market in 2019, the installed share of lithium iron phosphate was only 4.1%, rising slightly to 5.3% in 2020h1, and domestically produced in the second half of the yearTeslaModel 3, byadhan and other high-quality lithium iron phosphate models have been delivered successively, and the penetration rate of lithium iron phosphate in the passenger car market is expected to further improve.

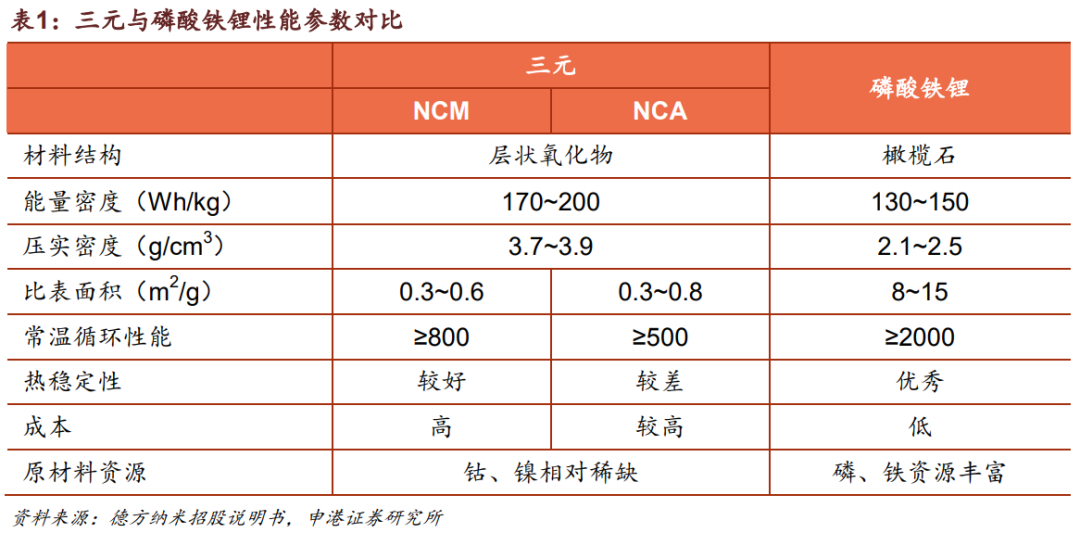

Ternary materials have high energy density, good magnification performance and excellent low-temperature performance, which are mainly used in medium and high-end passenger cars with high requirements for endurance mileage; Lithium iron phosphate has low energy density and poor low-temperature performance, which leads to obvious reduction of endurance mileage in winter, but it is low-cost and has good thermal stability. It is mainly used in passenger cars and basic passenger cars.

October iron phosphatelithium batteryThe direct reason for the continuous high increase in installed capacity is the hot sales of new models led by BYD Han EV and Wuling Hongguang Mini。 In October 2020, the installed capacity of power battery was 5.87gwh, with a year-on-year increase of 44%, of which the installed capacity of lithium iron phosphate was 2.41gwh, with a year-on-year increase of 127.5%. In October, Hongguang Mini sold 20631 vehicles, which continued to occupy the top place in vehicle sales. The product strategy of pricing 28800 yuan without new energy subsidies has been confirmed by the market. BYD has sold 5055 vehicles, with limited production capacity in the early stage and low delivery level. With the release of production capacity, terminal sales will gradually rise.

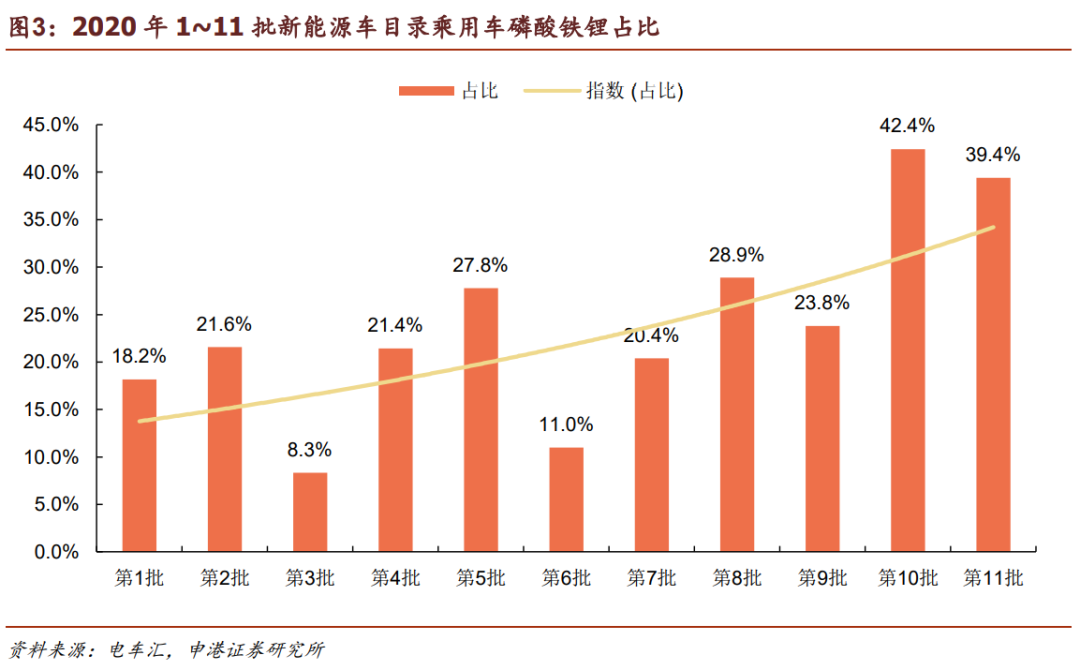

In the recommended catalogue released in 2020, iron phosphateLithium batteryThe pool supporting has been upgraded from the previous A00 model to the medium and high-end model, and is expected to seize the market share of some Sanyuan 523 batteries with the advantages of low cost and high safety.In the field of passenger cars, a0/a00 small cars (such as Wuling macro mini and Chery ant) are mainly lithium iron phosphate, and a/a and B models are currently mainly ternary. However, with the improvement of energy density brought by technological progress and the application of blade battery CTP technology, the endurance mileage is significantly improved, such as domestic Tesla Model 3, BYD Han and other models, the endurance mileage can reach 450 ~ 605km, and the penetration rate of lithium iron phosphate is increasing.

BYD Han's single car has a charging capacity of 76.9kwh. At present, the cumulative sales order has exceeded 40000 units. The domestic model 3 single car equipped with lithium iron phosphate supplied by Ningde times has a charging capacity of 55kwh. It has been officially delivered since September. The charging capacity of Wuling Hongguang Mini's two endurance versions is 14.4kwh (170km high endurance version) and 9.6kwh (120km low endurance version), respectively. As of October, the cumulative sales volume has reached 44000.It is expected that only the above three models will contribute about 5gwh of installed capacity to 2020h2 lithium iron phosphate passenger cars. Combined with the advantageous scale in the field of passenger cars and special vehicles, it is expected that the installed capacity of lithium iron phosphate will exceed 16gwh in the second half of the year.

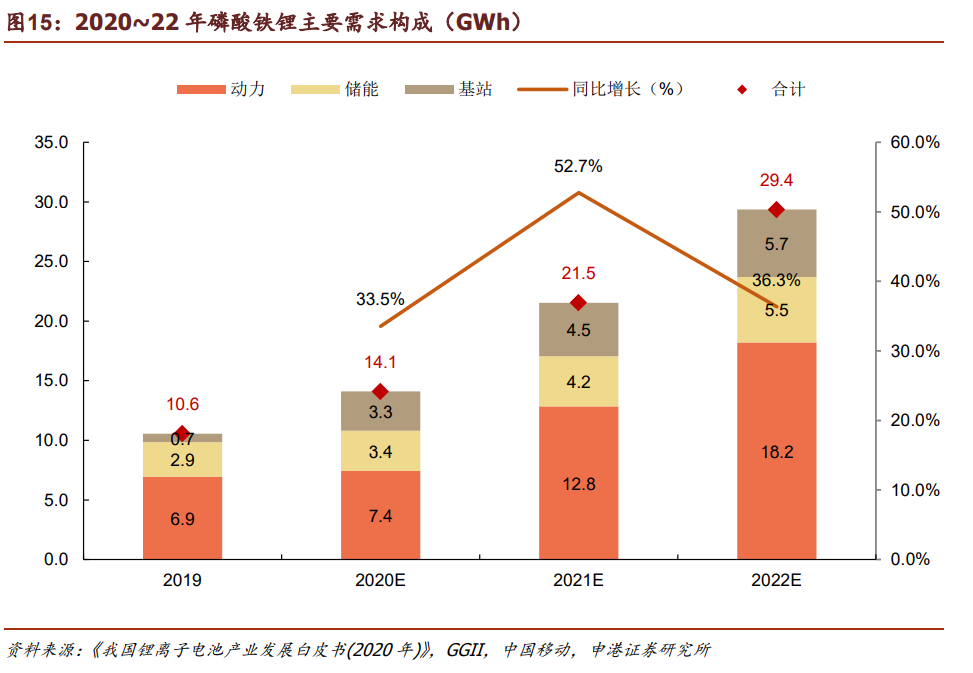

At present, the new energy vehicle market has returned to the growth track. It is expected that the annual sales volume will be basically the same as last year, and the compound growth rate in the next three years will maintain a high growth rate of more than 30%,It is estimated that the sales volume of new energy vehicles will be 1.2 million, 1.6 million and 2 million from 2020 to 22. At the same time, considering the increase in the penetration rate of lithium iron phosphate in the field of passenger cars and the increase in energy density, it is estimated that the installed demand of lithium iron phosphate will reach 22, 38 and 54gwh, with a year-on-year increase of 7%, 72% and 42%.

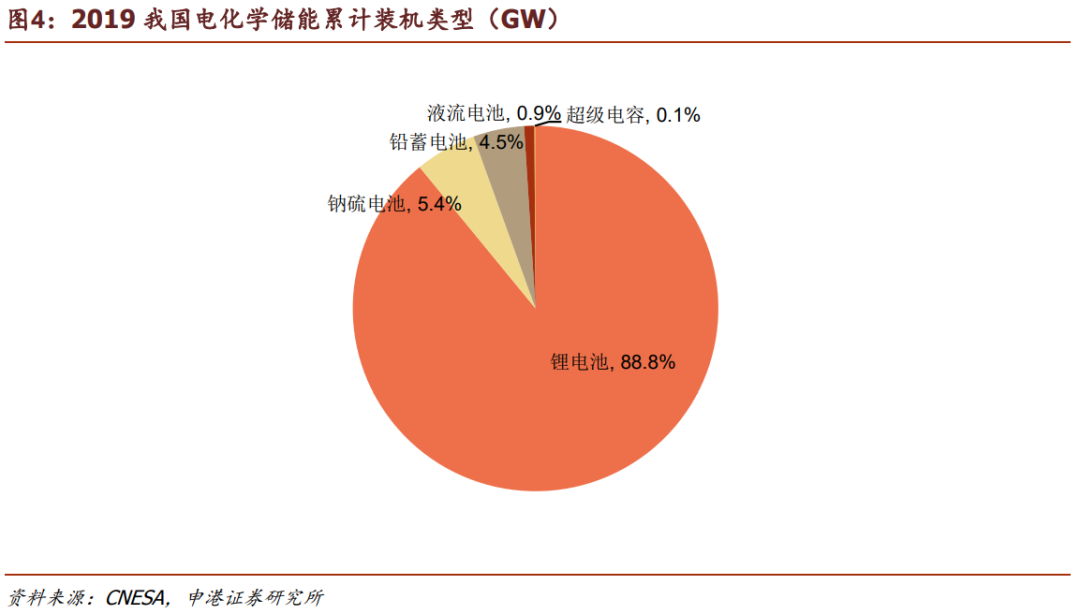

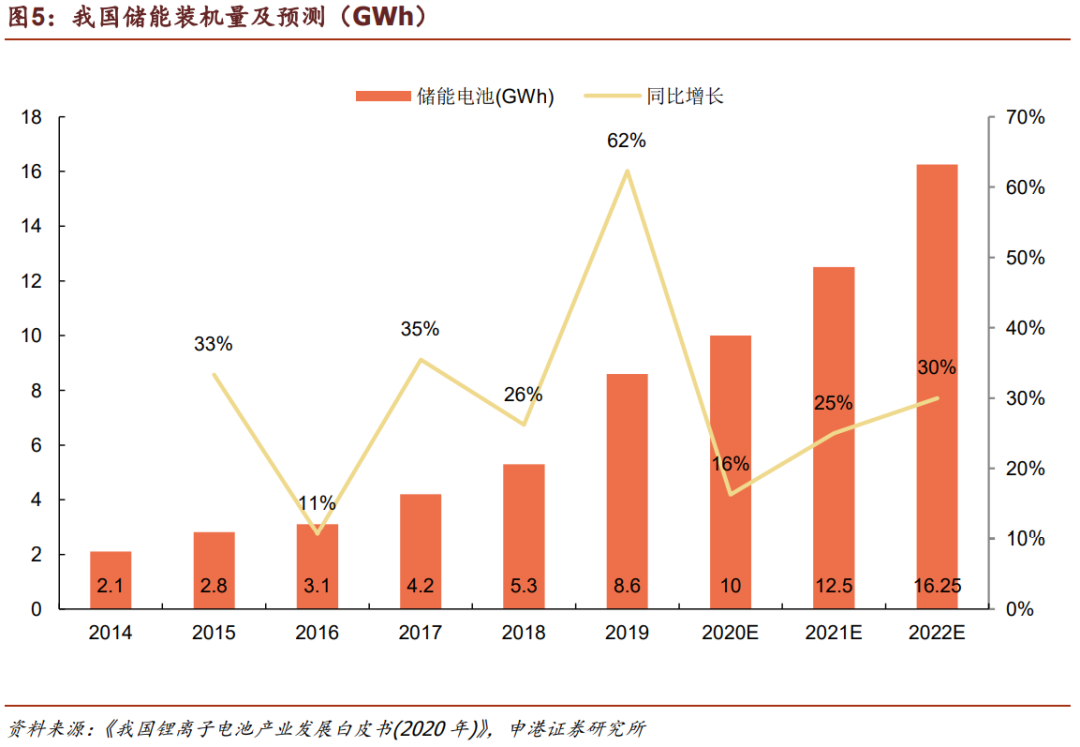

Lithium iron phosphate is the most suitable electrochemical technology route for energy storage power stations at present。 With the continuous decline of the cost of lithium batteries and gradually approaching the economic inflection point of the application of energy storage systems, the energy storage market has great potential for development in the future. Lithium batteries are the mainstream in the field of power grid energy storage. By 2019, lithium batteries account for 88.8% of power station energy storage in China, and lithium iron phosphate technology is the main route.

With the large-scale growth of renewable energy power stations and the increase of the proportion of access to the power grid, combined with the construction of new energy vehicle charging network, the energy storage demand market will become broader. In 2019, China's new installed energy storage capacity was 8.6gwh, with a year-on-year increase of 62.3%.It is estimated that the lithium battery market for energy storage will grow at an average annual rate of 25% in the next three years, and the installed capacity will reach 10, 12.5 and 16gwh from 2020 to 22, with a year-on-year increase of 16%, 25% and 30%.

5g base station contributes to the new growth point of lithium iron phosphate demand in 2020。 In 2018, the number of global communication towers was about 4.3 million. In 2019, the construction of 5g base stations in China was rapidly started, with 150000 new ones. In 2020, the centralized purchase of 5g base stations announced by China's three major operators involved 520000 5g base stations: 270000 by China Mobile, and 250000 by Chinatelecom and China Unicom through joint networking.

On March 4, China Mobile announced that it plans to purchase a total of 610.2 million ah (about 1.95gwh) of lithium iron phosphate batteries for communications that do not exceed 2.508 billion yuan;

On March 11, China Tower announced the purchase of 5g lithium iron phosphate batteries for base stations, with a scale of about 2gwh.

With the gradual rise of 5g networks in the world, 2020-2025 will be a period of rapid growth of 5g base stations. A total of 410000 5g base stations have been opened in June 2020. It is expected that 700000 new and upgraded 5g base stations will be added in 2020, with a total number of 850000 base stations. The average annual growth rate of 30% will be maintained in the next three years, and 950000 and 1.2 million new base stations will be added from 2021 to 22.

The single station power consumption of traditional 4G base stations is about 780 ~ 930W. According to the public data of the head manufacturer, 5g base stations will reach about 3500W. Calculated according to the emergency duration of 4h,From 2020 to 22, the demand for lithium iron phosphate from 5g new base stations will reach 10, 13 and 17gwh respectively, with a year-on-year increase of 33.5%, 35.6% and 26.3%.

1.2 the price of lithium iron phosphate bottomed out and rebounded

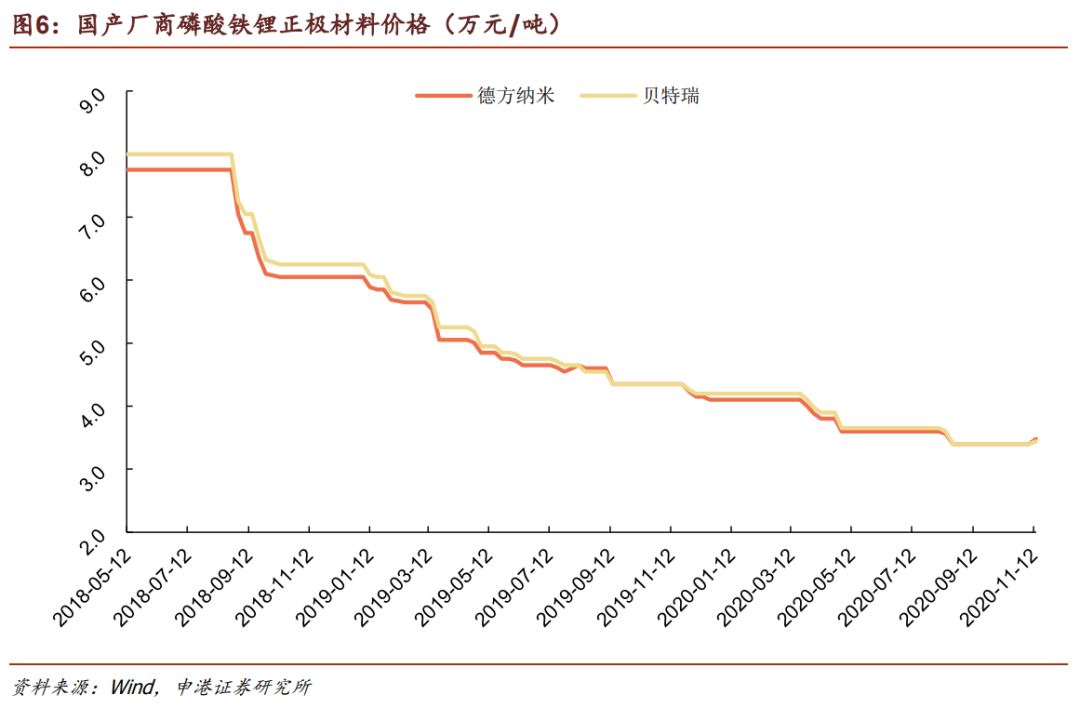

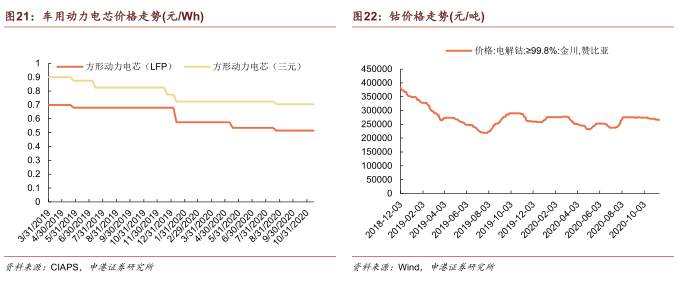

In recent years, the new energy vehicle industry has developed rapidly, the power battery industry chain has been maturing, the market-oriented competition pattern has become clearer, the competition among enterprises has intensified, and the price of cathode materials has continued to decline. The price of lithium iron phosphate cathode material has fallen continuously since the high of 80000 yuan / ton in 2018, reaching the lowest point of 34000 yuan / ton in 2020q3, a decrease of 57.5%. It rebounded slightly in November, with an increase of 3 ~ 6% according to the quotations of some mainstream manufacturers.

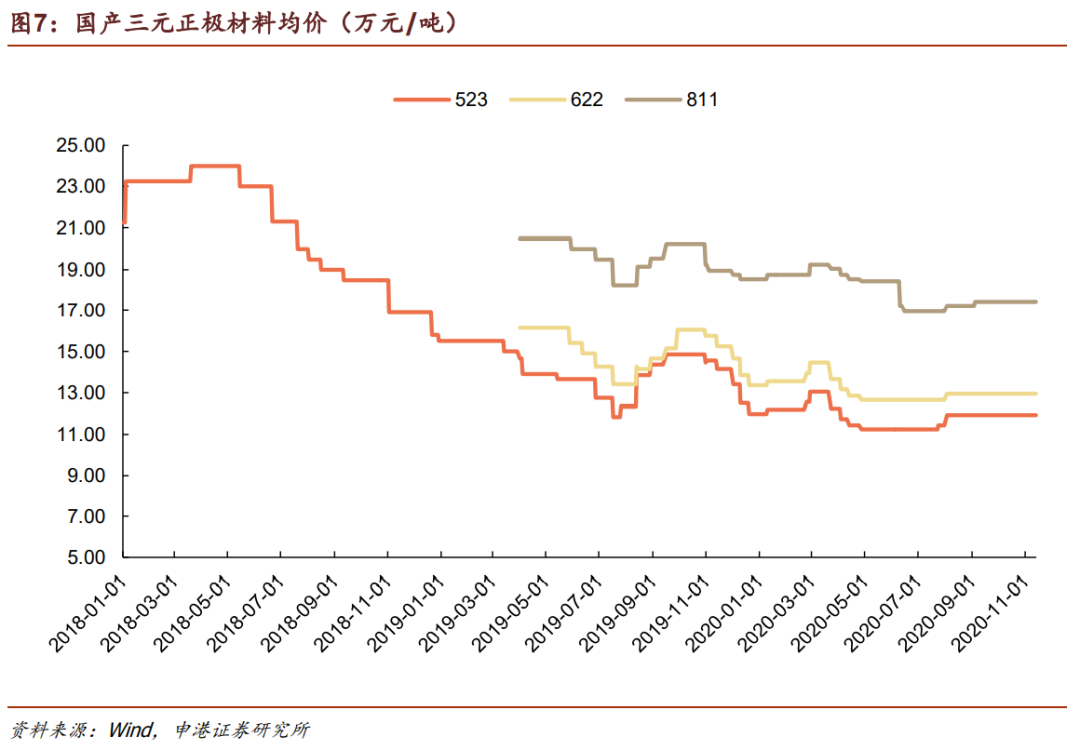

The price of ternary cathode material reached a high price of 240000 yuan / ton in 2018q2, and then fell. It has basically remained in a relatively stable price range since 2019, fluctuated slightly, and the downward trend has slowed down. The recent price has fallen by 50% compared with the peak in 2018.

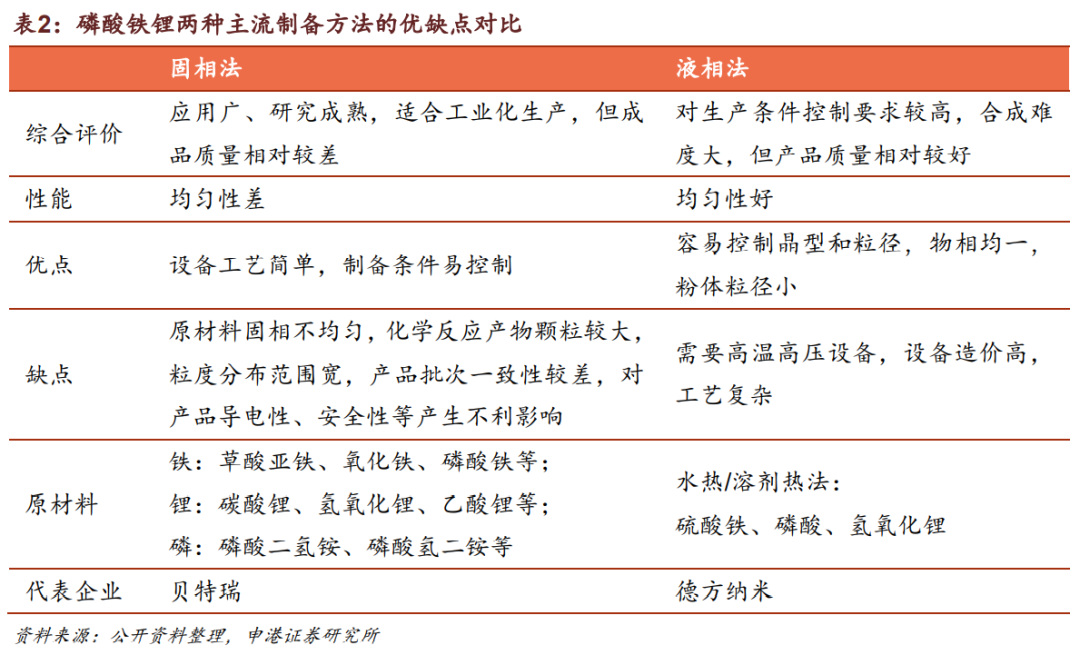

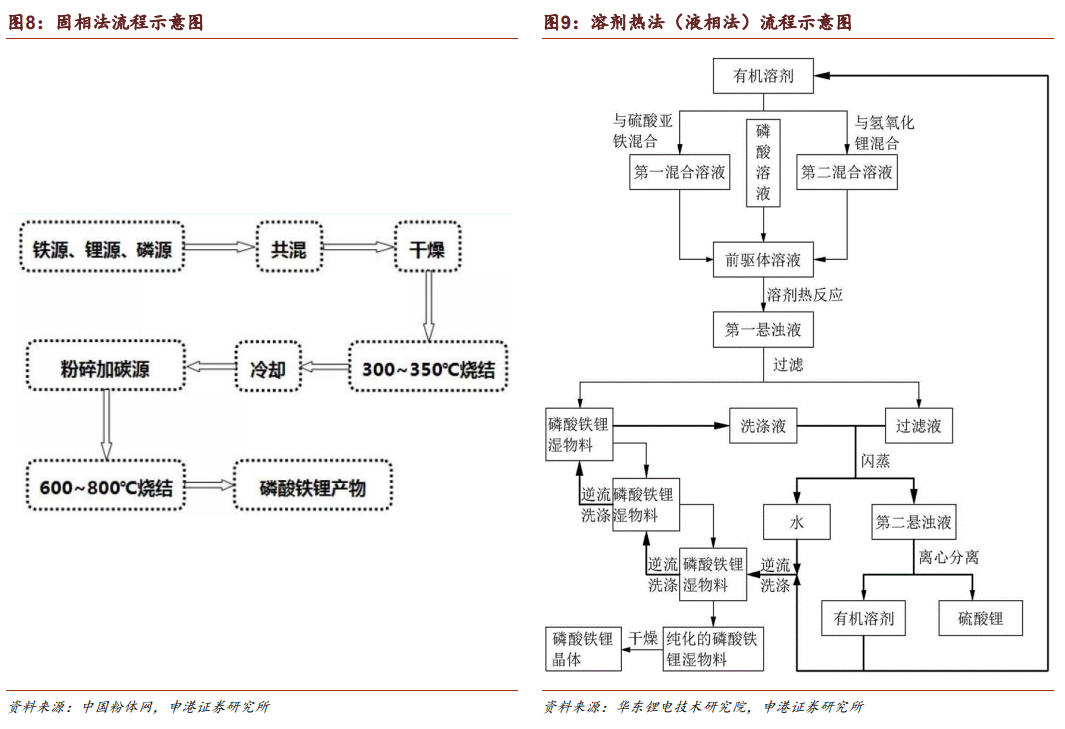

The production technology of lithium iron phosphate can be roughly divided into solid-phase synthesis and liquid-phase synthesis. The advantages of solid-phase process are prominent, and the quality of liquid-phase products is high:

The solid-phase method has many applications and mature technology, among which the carbothermal reduction method is the most widely used. The range of raw materials is relatively narrow, the equipment and process are relatively simple, and the preparation conditions are easy to control.

Because the raw materials of liquid phase method can be mixed at the molecular level, the products obtained by liquid phase method have more uniform mixing and better performance, but at the same time, the production conditions are more stringent.

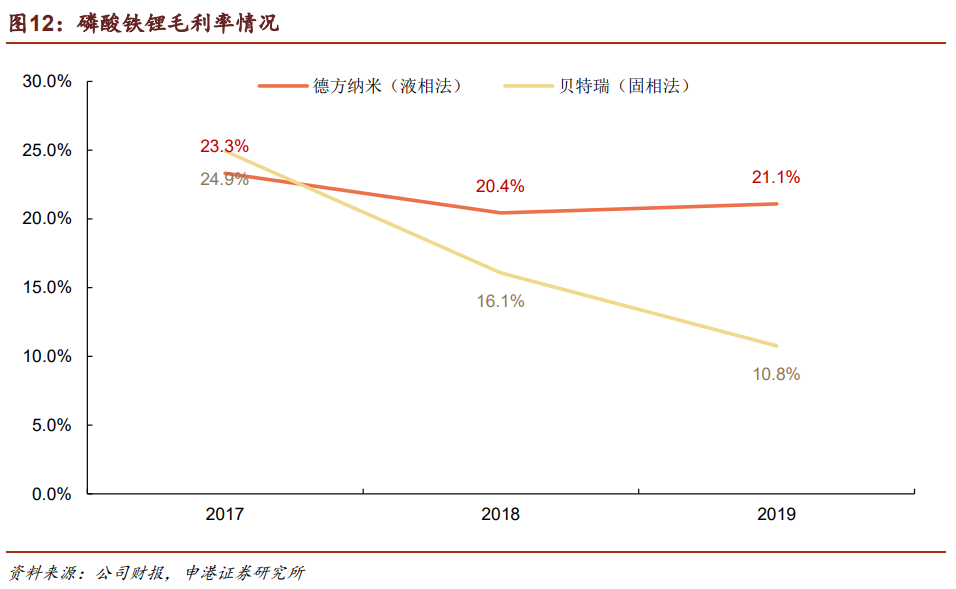

The equipment cost of liquid phase method is high and the process is complex, but the product quality is high. Therefore, manufacturers who choose liquid phase method need to constantly optimize the process to reduce the cost。 German nano, the leading manufacturer of lithium iron phosphate materials in China, chose the production route of liquid phase method, developed "self heating evaporation liquid phase synthesis method", reduced the production cost of precursor and sintering link, simplified the production process, effectively reduced the cost, and maintained a relatively stable gross profit rate while the unit price of lithium iron phosphate continued to decline.

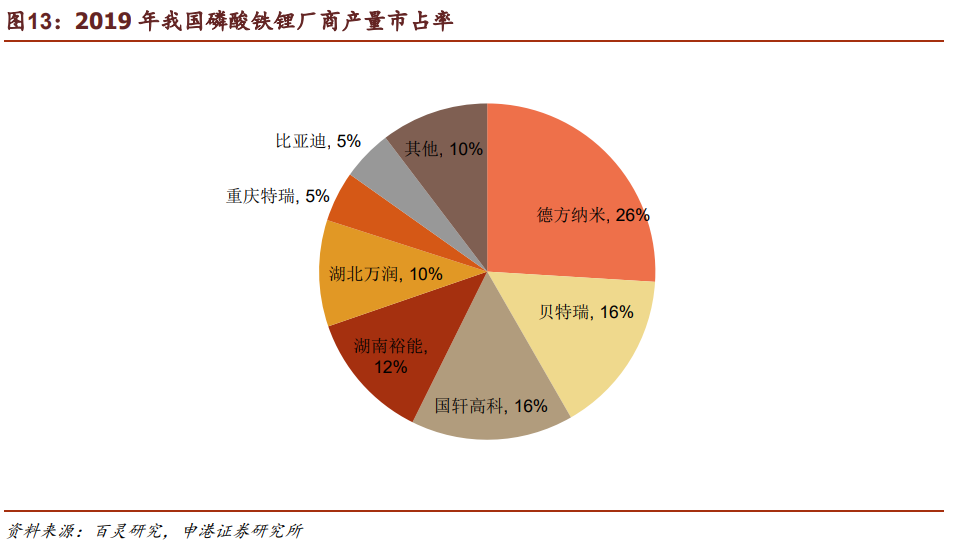

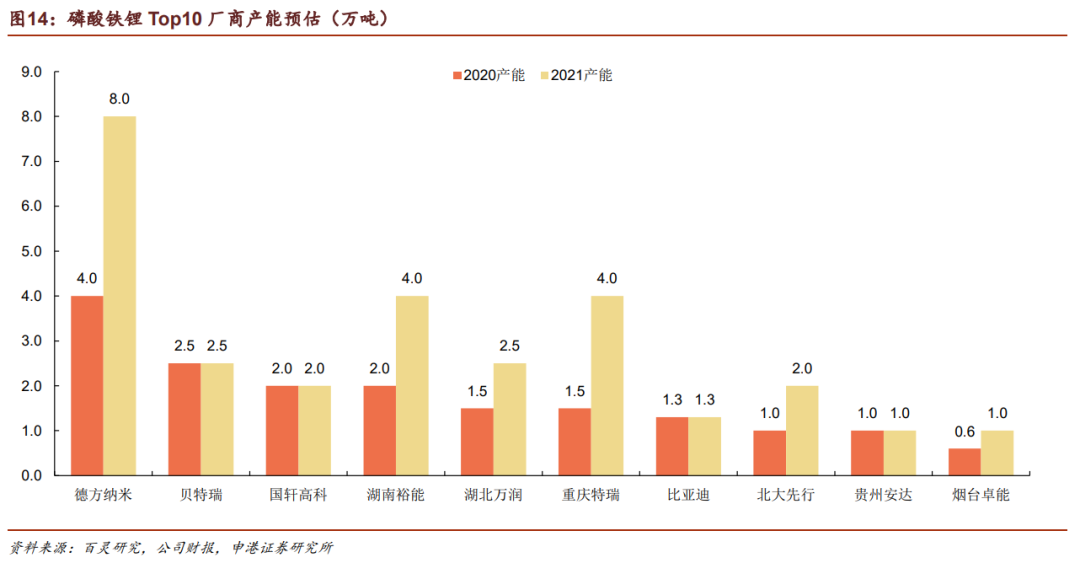

The lithium iron phosphate material industry has a high concentration, with the domestic market accounting for the top 10 manufacturers accounting for more than 95% of the national shipments. In 2019, the output of lithium iron phosphate materials in China was 92800 tons, and the output of German nano ranked first with 24000 tons, accounting for 26% of the market. After that, the output of beiteri and GuoXuan high tech was about 15000 tons, ranking second and third with a market share of 16%, of which GuoXuan high tech was mainly self supplied.

At present, the total capacity of the domestic industry is 180000 tons, and it is expected to reach 300000 tons by the end of 2021. At present, the leading manufacturer German nano has an annual capacity of 30000 tons of lithium iron phosphate, and another 35000 tons of capacity under construction. It is expected that the total capacity will be more than 40000 tons by the end of the year, and will reach 80000 tons in 2021.

The price of lithium iron phosphate rebounded from the bottom, and at the same time, the dual driving forces of direct demand increment and terminal application structure adjustment pushed up demand. Lithium iron phosphate will usher in a simultaneous rise in volume and price。 The penetration rate of lithium iron phosphate in domestic new energy vehicles and passenger cars has increased, the demand for energy storage and installation due to the rapid development of renewable energy power generation, and the accelerated construction of 5g base station passenger new infrastructure Dongfeng have become the main sources of demand for lithium iron phosphate in the future.

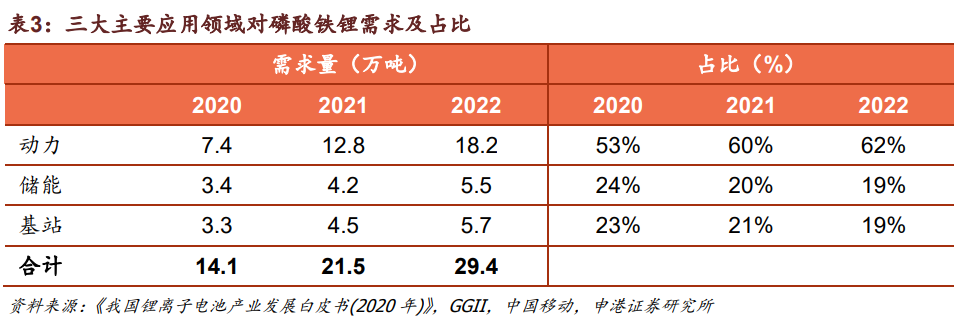

Based on the conversion relationship between lithium iron phosphate material and battery terminal demand in 2019, we predict that the demand for lithium iron phosphate will reach 141000, 215000 and 294000 tons from 2020 to 2022, with an annual compound growth rate of 41%. Among them, power batteries are the main growth force, accounting for about 60% of the total demand in the next three years, and energy storage and 5g base stations each account for 20%.

The lithium iron phosphate industry has been in a state of oversupply for a long time, but leading manufacturers are still actively expanding production. With the intensification of market-oriented competition for lithium batteries, high-quality manufacturers are expected to continue to expand market share by virtue of cost and technical advantages. It is recommended to pay attention to German nano meter, the leader of lithium iron phosphate material.

Investment summary

one

Market Review

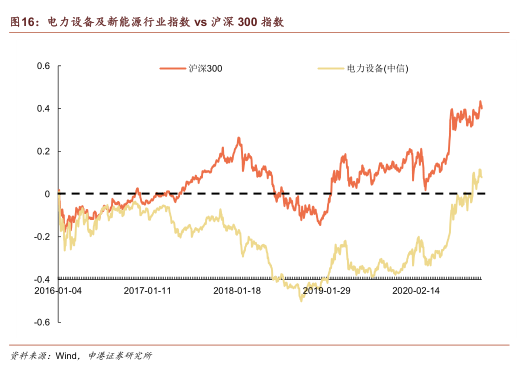

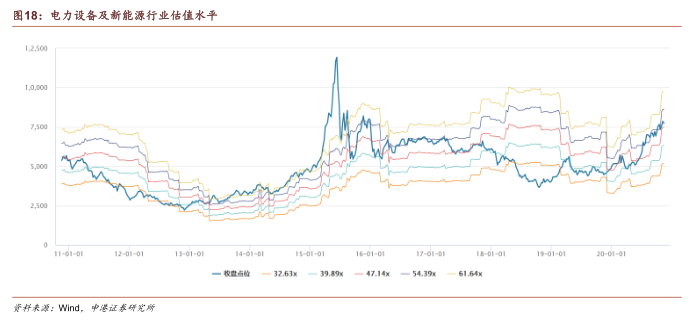

As of the close on November 13, the power equipment and new energy sector fell 1.53% this week, 0.94pct behind the Shanghai and Shenzhen 300 index. This week, it ranked 26th among the 30 sectors of CITIC, and its overall performance was in the downstream. From the perspective of valuation, the current industry as a whole is 48.81 times the level, which is at the historical median.

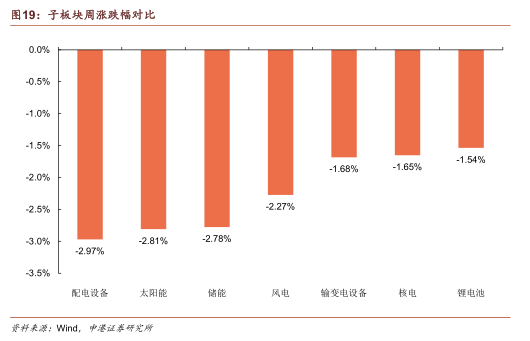

Gains and losses of sub sectors:Power distribution equipment (-2.97%), solar energy (-2.81%), energy storage (-2.78%), wind power (-2.27%), power transmission and transformation equipment (-1.68%), nuclear power (-1.65%), lithium battery (-1.54%).

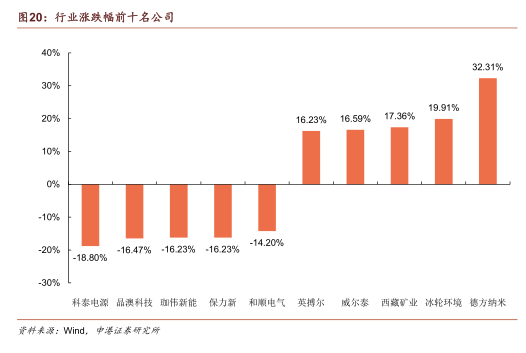

Top five stock price increases:German nano, ice wheel environment, Tibet Mining, wiltai, inger

Top five share price declines: Ketai power supply, Jingao technology, Jiawei Xinneng, baolixin, Heshun electric

two

Industry hotspot

New energy vehicles:In October, the sales volume of new energy passenger vehicles was 144000, 119.8% year-on-year and 15.9% month on month.

three

investment strategy

New energy vehicles:The State Council issued the new energy vehicle industry development plan (2021-2035). By 2025, the average power consumption of EV passenger vehicles will be reduced to 12kwh/ 100km, and the market share of new energy vehicles will reach 20%, promoting the electric transformation of the automotive industry. Price of lithium battery industry chain: fluctuations of cobalt based raw materials: cobalt powder (-0.4%), electrolytic cobalt (-0.4%); Lithium carbonate (0.3 ~ 1.4%), lithium iron phosphate (2.5%), optimistic about the trend of ternary high nickel and lithium battery globalization, it is recommended to pay attention to Ningde times, dangsheng technology, putailai, Enjie shares, Xinwangda

Photovoltaic:Price fluctuation of photovoltaic industry chain this week: imported polysilicon for single crystal (-1%); Imported single crystal perc battery chips and components increased slightly (1 ~ 1.8%); The price of photovoltaic glass is stable. It is optimistic that the industry concentration will increase and the anti risk ability of the leaders will highlight the trend after the end of the epidemic, and it is recommended that monocrystalline silicon materials and perc battery leading Tongwei shares and monocrystalline silicon leading Longji shares.

Wind power:State Grid predicts that the installed capacity of wind power is expected to exceed 30GW in 2020. Under the western development policy in the new era, the local consumption of renewable energy in the West and the construction of export channels have received key support. We are optimistic about Jinfeng technology, the leader of wind turbine manufacturers, Tianshun wind energy, the leader of wind tower, and Sinoma technology, the leader of fan blades.

Grid investment:UHV will become an important direction of power grid investment. It is planned to invest 181.1 billion in 2020 to ensure the completion of the "three AC and one DC" project within the year. The countercyclical property of power grid investment has been valued by the market, and there is great room for development. We are optimistic about Nari, the leader of power grid automation, and sinonet, the leader of power grid informatization

four

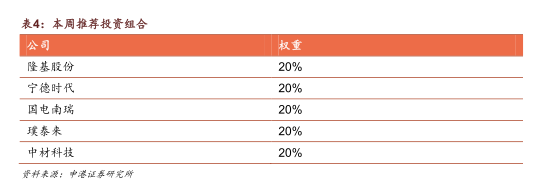

investment portfolio

Longji shares, Ningde times, Guodian Nari, putailai, Sinoma technology 20% each.

five

Risk statement

The sales volume of new energy vehicles is less than expected; The installed capacity of new energy power generation is less than expected; Material prices fell more than expected; The approval of nuclear power projects did not meet expectations.

Report body

one

Industry hot news

In October, the sales volume of new energy passenger vehicles was 144000, with a year-on-year increase of 119.8% and a month on month increase of 15.9%。 The passenger Federation released the sales data of new energy passenger vehicles in October. The wholesale sales exceeded 144000, with a year-on-year increase of 119.8% and a month on month increase of 15.9%. Among them, the sales volume of plug-in hybrid vehicles was 23000, with a year-on-year increase of 58.6%, and the wholesale sales volume of pure electric vehicles was 121000, with a year-on-year increase of 137.2%. In October, the new energy passenger vehicle market was diversified, and the enterprises with sales exceeding 10000 vehicles included 29711 SAIC GM Wuling vehicles, 22395 BYD vehicles, 12785 SAIC passenger vehicles and 12143 Tesla China vehicles. Weilai, ideal, Weima, Xiaopeng, Hezhong, zero race and other new forces car enterprises are excellent. Great Wall Motors and GAC new energy also grew at a high speed, and the differentiation of new energy performance of large groups intensified. Among all electric vehicles, the A00 class accounts for 42% and the B class accounts for 21%. The model level is further differentiated under the current sales scale of new energy.

two

Investment strategy and key recommendations

New energy vehicles: 1) the State Council issued the new energy vehicle industry development plan (2021-2035), which mentioned that in 2025, the average power consumption of new EV passenger vehicles will be reduced to 12kwh/ 100km, and the new market share of new energy vehicles will reach about 20%, guiding the orderly development of the new energy vehicle industry. 2) The subsidy for new energy vehicles will be extended to the end of 2022, and the subsidy standards from 2020 to 2022 will decline by 10%, 20%, 30% and more than 300000 yuan respectively from the previous yearElectric vehicleSubsidies will not be granted. 3) A number of departments and domestic new energy vehicle enterprises jointly launched new energy vehicles to the countryside, which will promote the expansion of the middle and low-end new energy vehicle market. 4) During the epidemic, there was great downward pressure on the economy, and the new infrastructure became an important driver of the economy. As of September 2020, there were 606000 public charging piles, including 350000 AC charging piles and 255000 DC charging piles. As an important part of the new infrastructure, charging piles were mentioned in the 2020 government work report, which will usher in the acceleration of investment. It is expected that the investment in the charging pile industry will be about 10billion yuan in 2020.Price changes in the lithium battery industry chain this week: the prices of cylindrical and square lithium batteries remained stable. The price fluctuation of upstream cobalt series raw materials: cobalt powder (-0.35%), electrolytic cobalt (-0.37%), and the price of cobalt sulfate increased (3.74%); Lithium hexafluorophosphate stabilized, lithium carbonate continued to rise (0.27 ~ 1.43%), the price of ternary precursor remained stable, the price of lithium iron phosphate in cathode material increased (2.46%), and the prices of cathode material, diaphragm and electrolyte remained stable. We are optimistic about the trend of high energy density, ternary high nickel and lithium battery globalization. We recommend paying attention to Ningde times, dangsheng technology, putailai, Enjie shares and Xinwangda

Photovoltaic: 1) in 2020, the implementation of policies will be accelerated, the development path will be clear, and bidding projects will be implemented, with a total scale of 26gw exceeding expectations, which will drive Q3 domestic demand. 2) Affected by the epidemic, the project operating rate has decreased, the downturn in overseas demand is recovering, and the prices of products in all links have rebounded slightly. 3) The price of photovoltaic glass continued to rise sharply. The peak of module installation began in the second half of the year, and the penetration rate of double-sided modules continued to increase.Price fluctuation of photovoltaic industry chain this week: silicon material: the price of imported polysilicon single crystal fell slightly (-0.95%); The price of silicon wafer remained stable; The price of imported single crystal perc cells increased slightly (1.63 ~ 1.77%), the price of imported single crystal modules increased slightly (1.02 ~ 1.46%), and the price of photovoltaic glass remained stable. We are optimistic about the industry trend of improving industry concentration and highlighting the anti risk ability of leading enterprises after the end of the epidemic, and recommend monocrystalline silicon materials and perc battery leading Tongwei shares and monocrystalline silicon leading Longji shares.

Wind power:From January to September 2020, the wind power generation was 297.2 billion kwh, with a year-on-year increase of 15.8%, and the growth rate increased by 10.7pct year-on-year. The red warning of wind power has been completely lifted, a large number of existing projects in Xinjiang and Gansu have been released, and domestic demand is strong. It is expected that the installed capacity of wind power is expected to exceed 30GW in 2020. The state has issued guidance to support the western development in the new era and strengthened the development and utilization of renewable energy. Wind power and photovoltaic will usher in new development opportunities. The report "China's wind power industry map 2019" was officially released. In 2019, the new installed capacity of China's decentralized wind power (decentralized, distributed, intelligent microgrid) was 300MW, with a year-on-year increase of 114.8%. We are optimistic about Jinfeng technology, the leader of wind turbine manufacturers, Tianshun wind energy, the leader of wind tower, and Sinoma technology, the leader of fan blades.

Grid investment:The State Grid has experienced leadership changes, and the emphasis on UHV has been increasing. UHV will become an important direction of power grid investment. It is planned to invest 181.1 billion in UHV in 2020 to ensure the completion of the "three AC and one DC" project within the year. In addition, China has successfully implemented live working on 750 kV transmission lines in high altitude areas for the first time. The countercyclical nature of power grid investment has been valued by the market. The countercyclical operation in 2020 will be an important driver of a stable economy, and power investment has room for development. We are optimistic about Nari, the leader of power grid automation, and sinonet, the leader of power grid informatization.

Nuclear power:From January to September 2020, the nuclear power generation capacity was 270 billion kwh, with a year-on-year increase of 6.4%, the growth rate fell by 14.7pct year-on-year, and the utilization hours of power generation was 5521 hours, an increase of 69 hours over the same period of the previous year. By the end of September this year, China had 48 nuclear power units in operation, with a total installed capacity of 49.88 million KW; There are 14 nuclear power units under construction, with a total installed capacity of 15.53 million KW. Changjiang nuclear power phase II and san'ao nuclear power phase I were approved, and the total effective investment of the two projects exceeded 70billion yuan. Overseas, Poland's first nuclear power unit is planned to be put into operation before 2033, and South Korea plans to build apr-1400 units in Ukraine. The steam turbine contracts of CNNC Tianwan No. 7, No. 8, xudabao No. 3 and No. 4 nuclear power units have been signed, and the construction will start at the end of this year and the middle of next year respectively. We are optimistic about China nuclear power, Jiuli special materials and Yingliu, the leading enterprises in the industrial chain.

Power supply and demand:From January to September 2020, the total electricity consumption of the whole society was 5413.4 billion kwh, with a year-on-year increase of 1.29%, and the growth rate fell by 3.37 PCT compared with the same period last year. In 2019, non fossil energy power generation increased rapidly, including thermal power (1.9%), wind power (7%), hydropower (4.8%), photovoltaic (13.3%), nuclear power (18.3%). The demand side grew steadily, while the supply side showed a clean and efficient trend. We are optimistic about nuclear power and wind power operating enterprises with fixed costs and marginal costs of almost zero, and recommend China nuclear power and Funeng.

Energy storage:The national development and Reform Commission has officially defined the scope of new infrastructure. Thanks to this, the "land subsidy" policy for charging piles has been intensively introduced. It is expected to complete an investment of about 10billion yuan this year, with 200000 new public piles, more than 400000 new private piles, and 48000 new public charging stations. China's electrochemical energy storage capacity has reached 1.7 million KW, and it is expected that the energy storage market will continue to grow steadily in the next few years. The Ministry of industry and information technology announced the fifth batch《Lithium ion batteryA total of 15 battery enterprises were selected from the list of enterprises in the industry standard conditions. We are optimistic about green beauty, the leader in the waste battery recycling industry.

Our recommended portfolio this week is as follows:

three

Market Review

As of the closing on November 13, the power equipment and new energy sector fell 1.53% this week, the Shanghai and Shenzhen 300 index fell 0.59%, and the power equipment and new energy industry fell 0.94pct behind the Shanghai and Shenzhen 300 index.

From the perspective of sector ranking, compared with other sectors, the power equipment and new energy industry fell by 1.53% this week, ranking 26th among the 30 sectors of CITIC, and the overall performance is in the downstream.

From the perspective of valuation, the overall power equipment and new energy industry has fluctuated slightly recently, with the current level of 48.81, which is at the historical median.

In terms of sub sectors, the power distribution equipment sector fell by 2.97%, the solar energy sector fell by 2.81%, the energy storage sector fell by 2.78%, the wind power sector fell by 2.27%, the power transmission and transformation equipment sector fell by 1.68%, the nuclear power sector fell by 1.65%, and the lithium battery sector fell by 1.54%.

The top five stock price increases were German nano, ice wheel environment, Tibet Mining, wiltai, and inger.

The top five stock price declines were Ketai power, Jingao technology, Jiawei Xinneng, baolixin and Heshun electric.

four

Industry data

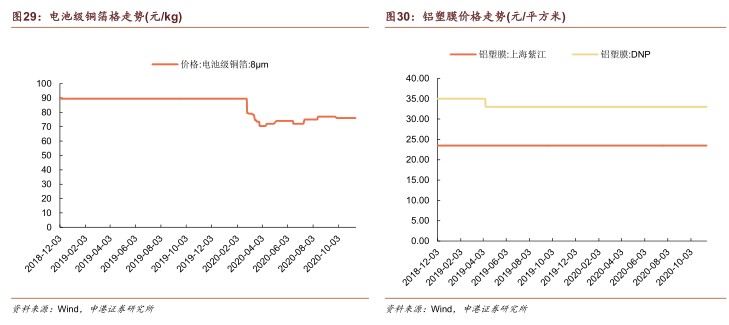

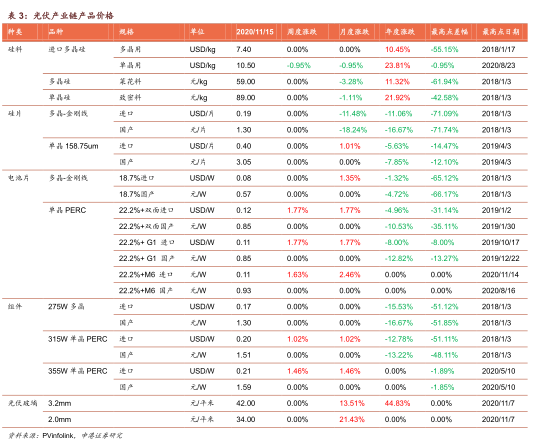

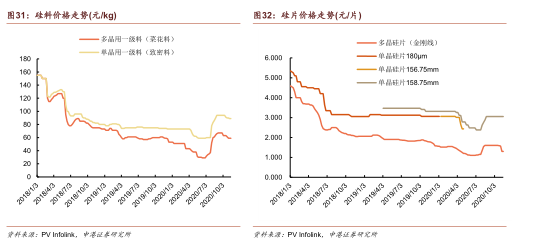

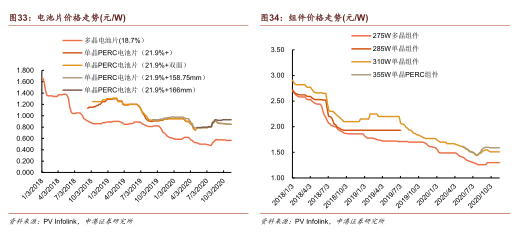

4.1 material price data of lithium battery industry chain

4.2 material price data of photovoltaic industry chain

five

Power supply and demand

5.1 power consumption of the whole society

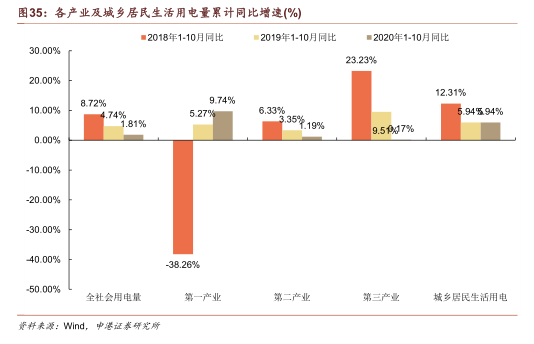

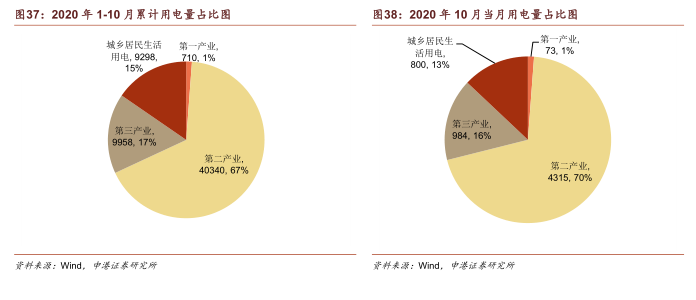

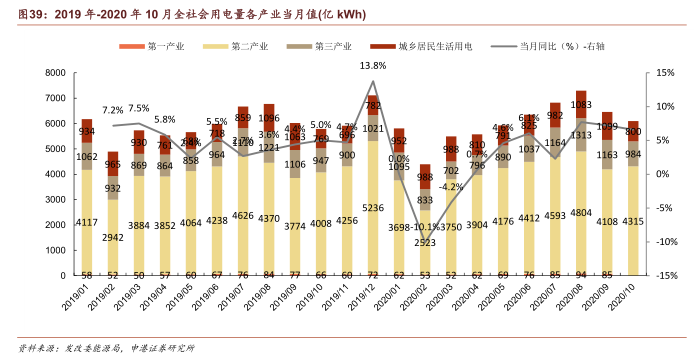

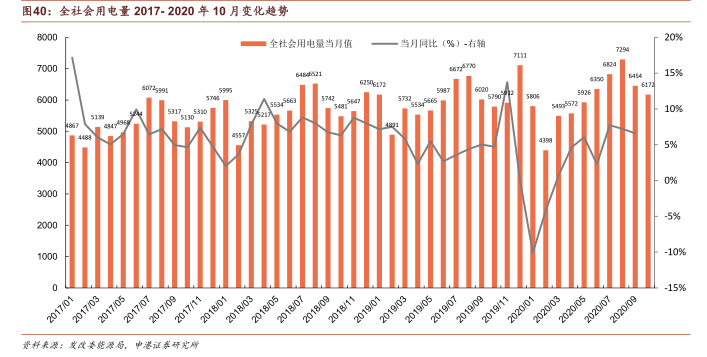

From January to October 2020, the total electricity consumption of the whole society was 6030.6 billion kwh, with a year-on-year increase of 1.81%, and the growth rate fell by 2.93 PCT compared with the same period last year. From the perspective of various industries and domestic power consumption of urban and rural residents:

The electricity consumption of the primary industry was 71 billion kwh, with a year-on-year increase of 9.74%, and the growth rate increased by 4.46pct year-on-year.

The electricity consumption of the secondary industry was 4034 billion kwh, with a year-on-year increase of 1.19%, and the growth rate fell by 2.16pct year-on-year.

The electricity consumption of the tertiary industry was 995.8 billion kwh, with a year-on-year increase of 0.17%, and the growth rate fell by 9.33pct year-on-year.

The domestic electricity consumption of urban and rural residents was 929.8 billion kwh, with a year-on-year increase of 5.94%, and the growth rate fell by 0.01 PCT year-on-year.

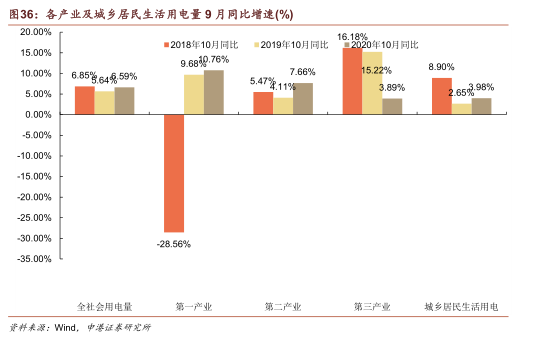

In October, the electricity consumption of the whole country was 617.2 billion kwh, with a year-on-year increase of 6.59%, and the growth rate increased by 0.96pct over the same period last year. From the perspective of various industries and domestic power consumption of urban and rural residents:

The electricity consumption of the primary industry was 7.3 billion kwh, with a year-on-year increase of 10.76%, and the growth rate increased by 1.08pct year-on-year

The electricity consumption of the secondary industry was 431.5 billion kwh, with a year-on-year increase of 7.66%, and the growth rate increased by 3.55pct year-on-year.

The electricity consumption of the tertiary industry was 98.4 billion kwh, with a year-on-year increase of 3.89%, and the growth rate decreased by 11.33pct year-on-year.

The domestic electricity consumption of urban and rural residents was 80billion kwh, with a year-on-year increase of 3.98%, and the growth rate increased by 1.33pct year-on-year.

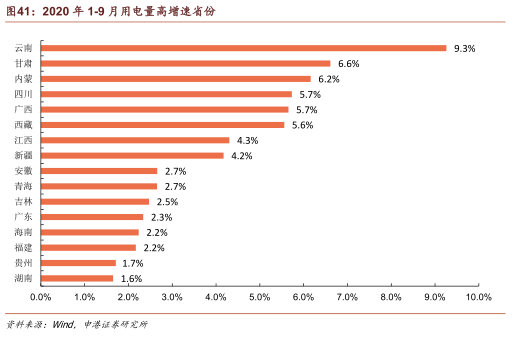

In terms of provinces, from January to September 2020, the electricity consumption of the whole society in most provinces increased. Among them, there are 16 provinces where the growth rate of electricity consumption in the whole society is higher than the national average (1.48%), and the top four provinces are Yunnan (9.3%), Gansu (6.6%), Inner Mongolia (6.2%), Tibet (5.7%), and Guangxi (5.7%).

5.2 renewable energy power generation

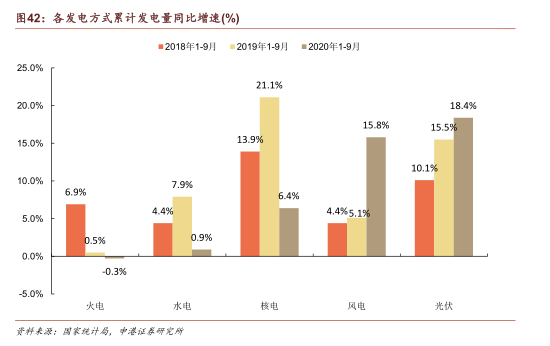

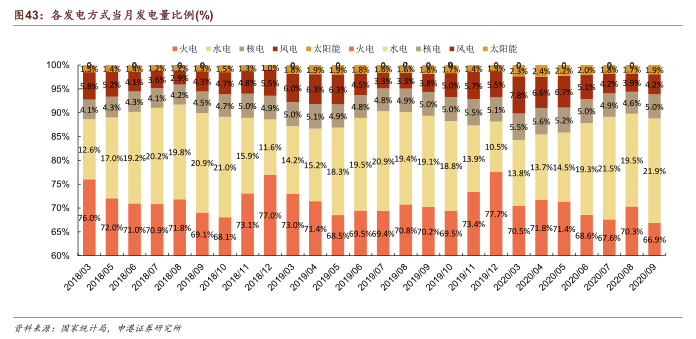

From January to September 2020, the national power generation was 5408.6 billion kwh, with a year-on-year increase of 0.9%, and the growth rate fell by 2.1pct compared with the same period last year. From the perspective of power generation capacity of various power generation methods:

Thermal power generation was 3831.6 billion kwh, a year-on-year decrease of 0.3%, and the growth rate fell by 0.7pct year-on-year.

Hydropower generation was 902.5 billion kwh, with a year-on-year increase of 0.9%, and the growth rate fell by 7.0 PCT year-on-year.

Nuclear power generation was 270 billion kwh, with a year-on-year increase of 6.4%, and the growth rate fell by 14.7pct year-on-year.

Wind power generation was 297.2 billion kwh, with a year-on-year increase of 15.8%, and the growth rate increased by 10.7pct year-on-year.

Photovoltaic power generation was 107.1 billion kwh, with a year-on-year increase of 18.4%, and the growth rate increased by 2.9pct year-on-year.

5.3 utilization hours of power generation

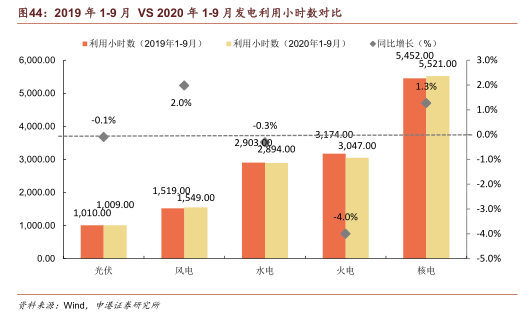

In terms of utilization hours of power generation, the cumulative average utilization hours of power generation equipment in China from January to September 2020 were 2758 hours, a decrease of 98 hours over the same period last year.

The average utilization hours of photovoltaic equipment across the country were 1009 hours, down 1 hour from the same period last year.

The average utilization hours of grid connected wind power equipment across the country was 1549 hours, an increase of 30 hours over the same period last year.

The average utilization hours of hydropower equipment in China were 2849 hours, a decrease of 9 hours over the same period last year.

The average utilization hours of thermal power equipment in China were 3047 hours, a decrease of 127 hours over the same period last year.

The average utilization hours of nuclear power equipment nationwide were 5521 hours, an increase of 69 hours over the same period last year.

5.4 renewable energy consumption

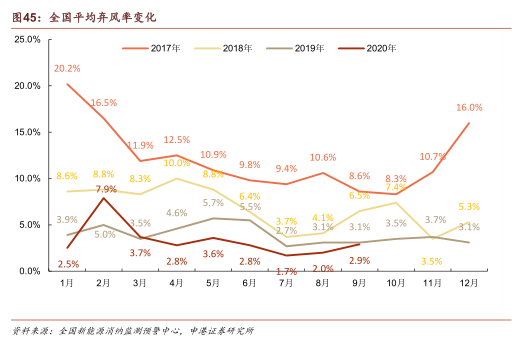

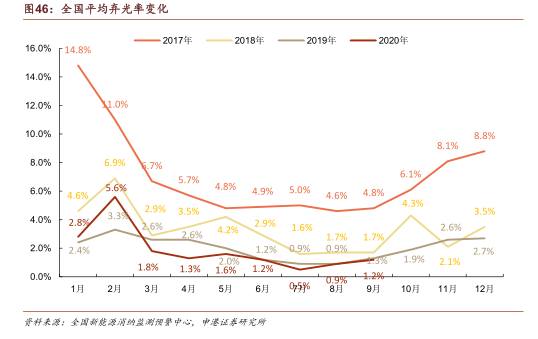

As the main body of new energy consumption, power grid plays a decisive role. According to the commitment of the State Grid, efforts will be made to control wind and light abandonment within 5% in 2020. The clean energy consumption action plan (2018-2020) issued by the energy administration requires that the wind rejection rate in 2020 should be less than 5%, and the light rejection rate should always be less than 5%.

The overall consumption and utilization of new energy across the country continued to improve. In the third quarter, the national waste air volume was 2.12 billion kwh, a year-on-year decrease of 10.6%, and the utilization rate of wind power was 97.8%, an increase of 0.8 percentage points year-on-year; The amount of light lost was 650million kwh, an increase of 1.6% year-on-year, and the utilization rate of photovoltaic power generation was 99.1%, an increase of 0.1 percentage points year-on-year. The consumption of new energy continued to be good.

Explore more new mechanisms for flexibly adjusting resources such as energy storage to promote the consumption of new energy. Major progress has been made in large-scale power transmission projects to promote clean energy consumption.

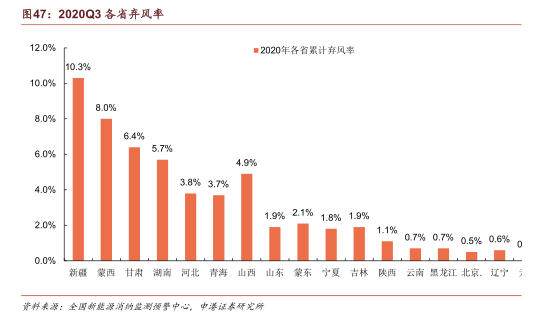

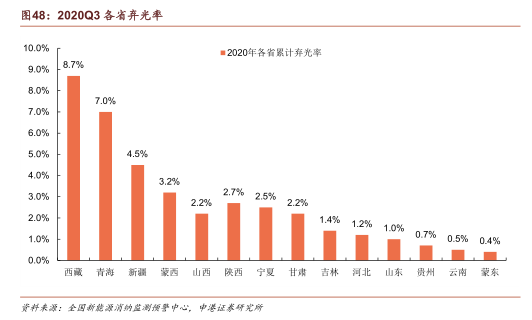

In 2020q3, the top three provinces with wind abandonment rate in China are Xinjiang (10.3%), Inner Mongolia Mengxi region (8.0%), and Gansu (6.4%). The top three provinces with light rejection rate are Tibet (8.7%), Qinghai (7.0%), and Xinjiang (4.5%).

six

6.1 production and sales of new energy vehicles

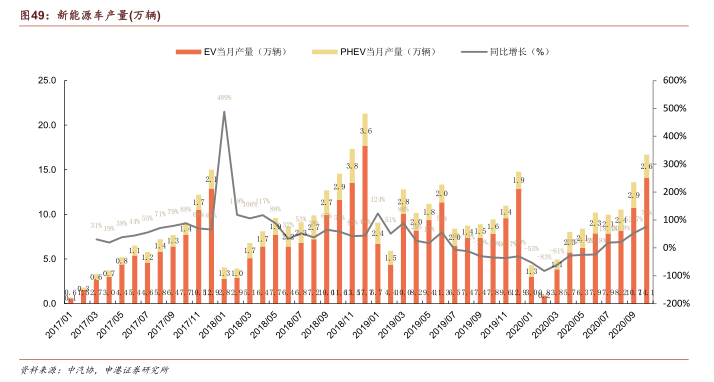

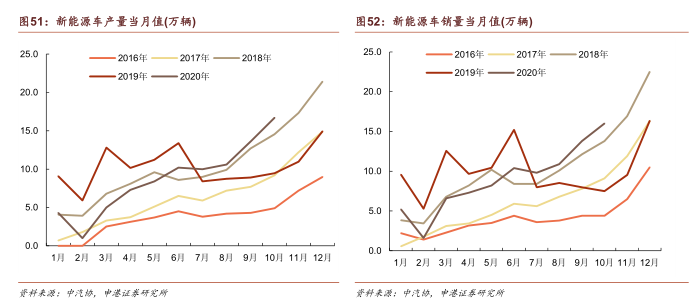

In October 2020, the output of new energy vehicles was 167000, with a year-on-year increase of 77% and a month on month increase of 22.74%, of which pureelectric vehicle141000 vehicles, with a year-on-year increase of 80%, and 26000 plug-in hybrid vehicles, with a year-on-year increase of 60%.

From January to October 2020, the cumulative output of new energy vehicles was 914000, a year-on-year decrease of 7.0%, including 719000 pure electric vehicles, a year-on-year decrease of 9.6%, and 195000 plug-in hybrid vehicles, a year-on-year decrease of 4.6%.

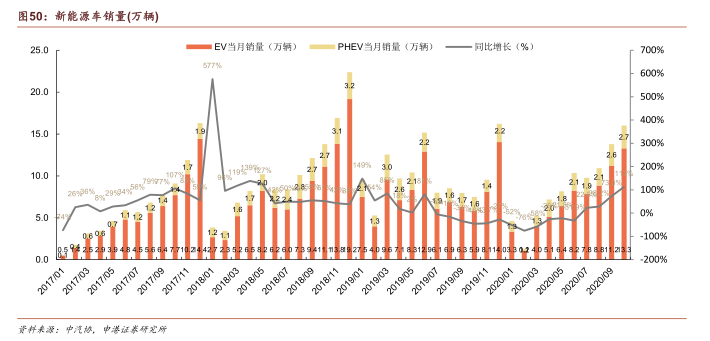

In October 2020, the sales volume of new energy vehicles was 160000, an increase of 113.0% year-on-year and 16.0% month on month. Among them, there were 133000 pure electric vehicles, a year-on-year increase of 127%, and 27000 plug-in hybrid vehicles, a year-on-year increase of 65.0%.

From January to October 2020, the cumulative sales volume of new energy vehicles was 901000, a year-on-year decrease of 4.9%, including 719000 pure electric vehicles, a year-on-year decrease of 4.2%, and 181000 plug-in hybrid vehicles, a year-on-year decrease of 7.5%.

6.2 power battery installation

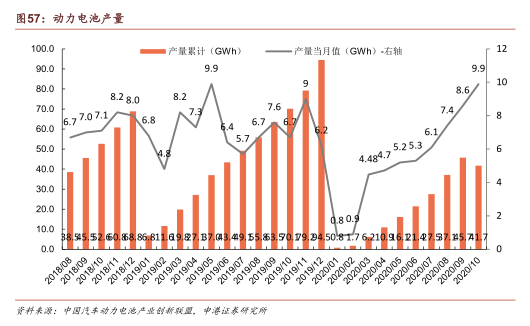

In October 2020, the installed capacity of power lithium battery was 5.9gwh, with a year-on-year increase of 44%. Among them, the installed capacity of ternary lithium battery is 3.4gwh, and the installed capacity of lithium iron phosphate battery is 2.4gwh.

From January to October 2020, the cumulative installed capacity of power lithium batteries was 40gwh, a year-on-year decrease of 13.3%. Among them, the cumulative installed capacity of ternary lithium battery is 27gwh, and the cumulative installed capacity of lithium iron phosphate battery is 12.8gwh.

In October 2020, the production of power batteries was 9.86gwh, with a year-on-year increase of 47.9% and a month on month increase of 14.5%. Among them, the output of ternary battery was 5.5gwh, with a year-on-year increase of 39.6% and a month on month increase of 16.1%; The output of lithium iron phosphate battery was 4.3gwh, with a year-on-year increase of 63% and a month on month increase of 12.6%.

From January to October 2020, the cumulative production of power batteries was 55.5gwh, a year-on-year decrease of 20.8%. Among them, the total output of ternary battery was 32.7gwh, a year-on-year decrease of 27.2%; The cumulative output of lithium iron phosphate battery was 22.6gwh, a year-on-year decrease of 1.2%.

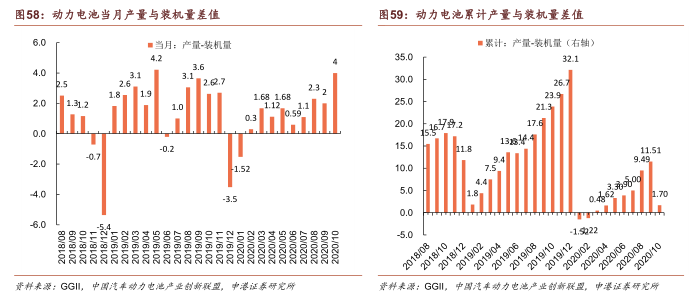

By calculating the difference between the output and installed capacity of power batteries, we can find that, driven by the gradual reduction of the negative impact of the epidemic and the wave of resumption of production, the output installed capacity from January to October 2020 is positive, indicating that this stage is in the stage of resumption of production, and the main power battery manufacturers have resumed production, with inventory accumulation.

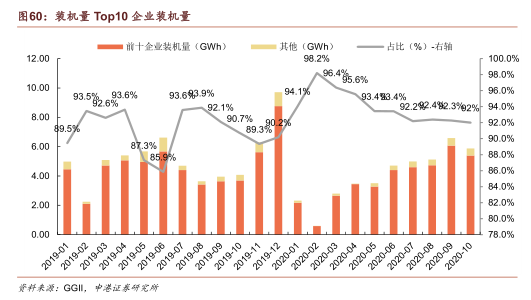

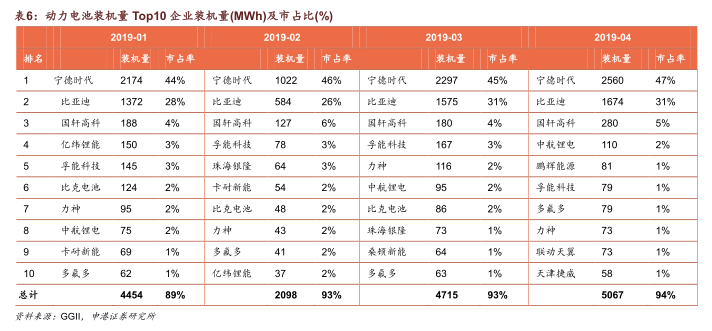

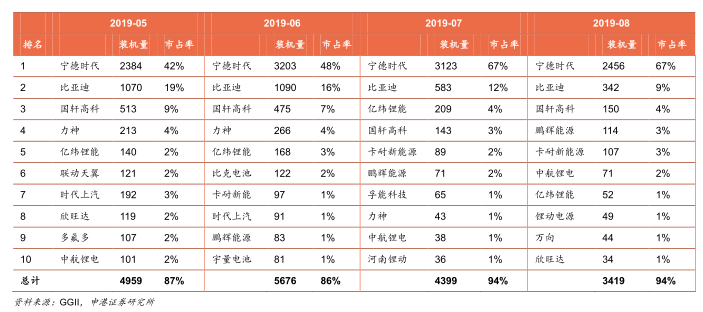

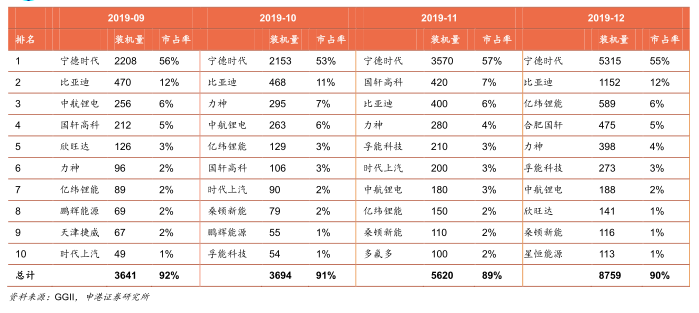

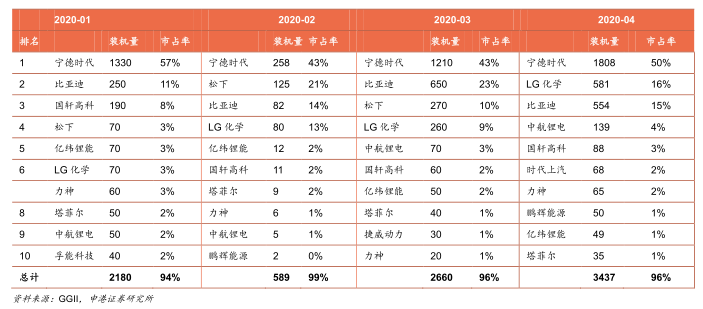

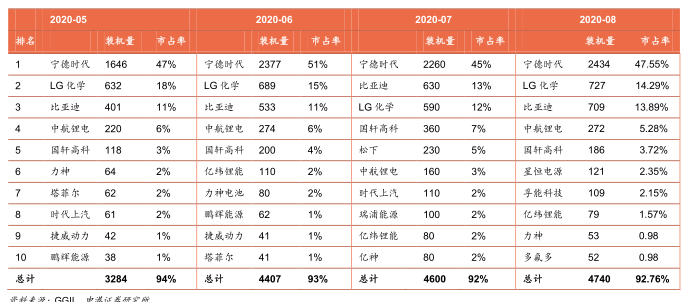

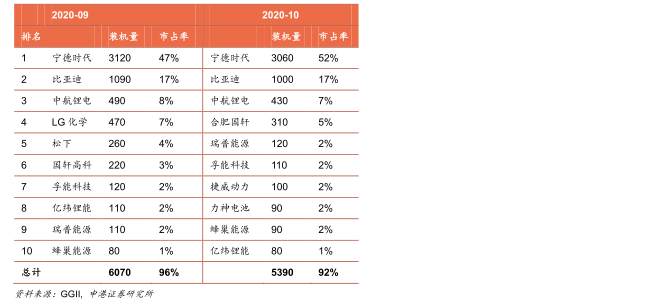

In October 2020, the market share of TOP10 power battery enterprises fluctuated occasionally, but remained basically stable. In October, the installed capacity of Ningde times accounted for 52.1%, and its leading position was stable. BYD rose to second place and AVIC lithium ranked third.

seven

Industry news

7.1 new energy vehicles

In October, the sales volume of new energy passenger vehicles was 144000, with a year-on-year increase of 119.8% and a month on month increase of 15.9%.The passenger Federation released the sales data of new energy passenger vehicles in October. The wholesale sales exceeded 144000, with a year-on-year increase of 119.8% and a month on month increase of 15.9%. Among them, the sales volume of plug-in hybrid vehicles was 23000, with a year-on-year increase of 58.6%, and the wholesale sales volume of pure electric vehicles was 121000, with a year-on-year increase of 137.2%. In October, the new energy passenger vehicle market was diversified, and the enterprises with sales exceeding 10000 vehicles included 29711 SAIC GM Wuling vehicles, 22395 BYD vehicles, 12785 SAIC passenger vehicles and 12143 Tesla China vehicles. Weilai, ideal, Weima, Xiaopeng, Hezhong, zero race and other new forces car enterprises are excellent. Great Wall Motors and GAC new energy also grew at a high speed, and the differentiation of new energy performance of large groups intensified. Among all electric vehicles, the A00 class accounts for 42% and the B class accounts for 21%. The model level is further differentiated under the current sales scale of new energy.

Equipment industry development center of the Ministry of industry and information technology: China's new energy vehicles have entered the stage of accelerated development.At the Forum on policies, regulations and standards system on the morning of November 12, Mr. Zuo Shiquan, director of the policy planning department of the equipment industry development center of the Ministry of industry and information technology, made a relevant interpretation of the new energy vehicle industry development plan 2035. At present, the development of new energy vehicles in China has entered the stage of accelerated development, leading the development of new energy vehicles in the world, and has achieved breakthroughs in market, technology and products. From the perspective of the situation, the development of new energy vehicles has injected new momentum into the world economy, and the integration of vehicles with relevant technologies in the fields of energy, transportation, information and communication has accelerated. Electrification, networking and intelligence have become the development trend of the automotive industry.

2020 World Conference on Intelligent connected vehicles: integrated development of intelligence and electrification。 On the afternoon of November 12, at the 2020 World Conference on Intelligent connected vehicles, many experts in the industry launched a dialogue on the theme of "the integrated development of intelligence and electrification", in-depth discussion on the new prospects of the development of intelligent connected vehicles and analysis of new problems. The theme of this conference is "new life of car service in the new era of intelligence". It aims to gather global elites to discuss the development prospects, discuss the construction of the ecological system of intelligent car service, cultivate new industrial formats, continue to lead the development trend of the global car industry, and start a new journey of comprehensively building a Chinese and even international standard intelligent car system.

7.2 photovoltaic

The Ministry of science and technology replied to the proposal on photovoltaic ecological restoration cooperation in the "the Belt and Road" countries.On November 9, the Ministry of science and technology replied to the "suggestions on photovoltaic ecological restoration cooperation in the" the Belt and Road "countries, pointing out that vigorously developing renewable energy has become a major strategic choice for global energy transformation and climate change response, and is a key factor for China to build a clean, low-carbon, safe and efficient energy system. While realizing the large-scale development and utilization of renewable energy such as photovoltaic power generation, strengthening the research on the impact and benefit of the ecological environment and giving full play to the positive role of photovoltaic power stations in the ecological restoration of desertification will provide a new path for the sustainable development of renewable energy industry.

Bidding announcement of national energy administration on research topics such as new energy consumption plan during the 14th Five Year Plan Period。 On November 12, the new energy department of the National Energy Administration issued a bidding announcement for four research topics, including the "Research on the national new energy consumption plan during the 14th five year plan" and the "Research on the management of industrial policies after the new energy parity is online". Tongwei signed a three-year 93000 ton polysilicon sales framework contract with Jingke energy.

7.3 wind power

Vestas has reached cooperation agreements with Zhangye City, Longyuan Power, PowerChina and TBEA.From November 5 to 6, Vestas wind technology (China) Co., Ltd. signed a series of cooperation agreements with Zhangye City, Longyuan Power Overseas Investment Co., Ltd., PowerChina Guizhou Engineering Co., Ltd., TBEA Xinjiang new energy Co., Ltd. and Shenneng Nanjing Energy Holding Co., Ltd. to further expand the renewable energy market and comprehensively help achieve China's 2060 carbon neutrality goal.

The first 30m offshore wind power professional operation and maintenance ship in China is planned to be put into operation next year。 On November 10, China shipbuilding group haizhuang Wind Power Co., Ltd. signed a contract with Yinghui Southern shipbuilding (Guangzhou Panyu) Co., Ltd. for the construction of offshore wind power professional operation and maintenance ship, marking the first offshore wind power operation and maintenance ship of China haizhuang entering the manufacturing stage. As the first 30 meter professional operation and maintenance ship in China, the ship will be officially put into operation at the end of 2021.

Hunan electric power wind energy equity restructuring Harbin Electric Group will take shares。 On November 12, Harbin Electric Power Group and Hunan Provincial People's government signed a strategic cooperation framework agreement in Changsha. According to the agreement, the two sides will carry out a series of cooperation in the equity restructuring of Xiangdian wind energy, the development of wind energy resources, the development of advanced equipment manufacturing industry, and the training of professional and technical personnel.

7.4 nuclear power

The first domestic high-efficiency subcritical circulating fluidized bed boiler was officially put into operation。 Recently, the first domestic 220t/h high-efficiency subcritical circulating fluidized bed boiler unit independently developed and designed by Dongfang Boiler was officially put into operation in Shandong Yiyuan yuanneng Thermal Power Co., Ltd. Yiyuan Xinjian 2 × The 50MW cogeneration project has been approved as one of the major practical projects for the transformation of new and old kinetic energy in Shandong Province. It is a key livelihood project at the municipal and county levels, and also a supporting energy center of Yiyuan chemical industry park. After the project is put into operation, it can reach the production scale of annual power generation of 1billion kwh, steam supply of 320 tons per hour, and the heating capacity will be increased by 7million square meters, which will effectively guarantee the heating demand in the urban area of Yiyuan County and provide preferential and stable power, steam and thermal energy support for the chemical industry park.

7.5 energy storage

Guangdong: build a smart grid that adapts to large-scale new energy access and meets the "plug and play" requirements of distributed energy.On November 5, the three-year implementation plan for promoting the construction of new infrastructure in Guangdong Province (2020-2022) was released, which pointed out that we should promote the ten smart projects and promote the construction of integrated infrastructure. Accelerate the construction of offshore wind power floating fan foundation platform, flexible DC centralized transmission, offshore hydrogen production, etc., and build a megawatt wave energy demonstration project. Accelerate the construction of intelligent substations and comprehensively improve the automation and intelligence level of distribution networks. By 2022, 10 new generation of "intelligent, modular and integrated" Smart Substation demonstration projects integrating power grid energy flow, business flow and information flow will be built.

7.6 power grid

The construction of the urban underground comprehensive pipe gallery project, the first 500kV EHV line in China, began.On November 5, "the first urban underground comprehensive pipe gallery of 500kV EHV line in China" - tanxinpei Road urban underground comprehensive pipe gallery and synchronous road lifting and reconstruction project started construction. The tanxinpei comprehensive pipe gallery project starts from Wuchang Avenue and ends at Miaoshan Avenue, with a total length of 6.25km. The 500kV high-voltage power project will bring the 500kV xiafeng I and II circuits from Wuchang avenue to Miaoshan avenue into the gallery, and synchronously transform the East-West overhead lines locally. The total construction period of the project is three years. After completion, it will be the first 500kV EHV line introduced into the urban integrated pipe gallery project in China, and it is also the world's longest underground 500kV Gil pipe gallery project.

eight

Listing announcement

8.1 main business trends

11-10

Bluestone reload:On November 9, 2020, Lanshi heavy equipment signed a shareholder contribution agreement with Chengdu Zhiyuan, and both parties intend to jointly invest to establish a joint venture Lanzhou Lanshi Zhiyuan Machinery Technology Co., Ltd. Lanshi heavy equipment invested 26.52 million yuan at the price of physical assets such as factory buildings, machinery and equipment, and held 51% equity of Lanshi Zhiyuan; Chengdu Zhiyuan invested 25.48 million yuan with intangible assets such as patent rights, trademark rights and non patented technology, and held 49% equity of Lanshi Zhiyuan.

Beijing Express:Beijing Jingyuntong Technology Co., Ltd. signed the investment agreement on 24gw single crystal pull rod and cutting project of Leshan Municipal People's government, Leshan Wutongqiao District People's government and Beijing Jingyuntong Technology Co., Ltd. with Leshan Municipal People's government and Leshan Wutongqiao District People's government, and reached a cooperation intention on the construction of 24gw single crystal pull rod and cutting project and related supporting facilities in Leshan WUTONGQIAO district. Leshan Municipal People's government designated hi-tech investment to jointly establish the project company with the company. The amount of contribution of hi-tech investment in the project company with industrial funds (funds) shall not exceed 1.2 billion yuan, and the company shall sign a guarantee contract to ensure the safety of funds after all contributions are made.

11-11

Current shares:On November 9, 2020, Huoshan Jiayuan Intelligent Manufacturing Co., Ltd., a wholly-owned subsidiary of Anhui Yingliu electromechanical Co., Ltd., invested to establish a wholly-owned subsidiary, Anhui Yingliu Materials Co., Ltd.

Pilot Intelligence:Wuxi leading intelligent equipment Co., Ltd. and its wholly-owned subsidiary Zhuhai Titan New Power Electronics Co., Ltd. successively received the notification of winning the bid from the main customer Ningde Times New Energy Technology Co., Ltd. and its holding subsidiaries via e-mail from September 21, 2020 to the disclosure date of the announcement. The total winning bid for lithium battery production equipment was about 3.228 billion yuan (excluding tax). The final transaction amount and project performance terms of this bid winning shall be subject to the formal contract.

Enjie shares:Yunnan Enjie new materials Co., Ltd. is a wholly-owned subsidiary semcorp Hungary korl á tolt felel? sség? T á RSAs á g, as the main body, invested in the construction of wet lithium battery isolation film production lines and supporting plants in Debrecen (Debrecen city), Hungary, mainly to carry out the manufacturing and sales of wet base film and functional coating diaphragm of lithium battery. The project plans to build four fully automatic imported film production lines and more than 30 coating production lines. The annual production capacity of base film is about 400million square meters, and the total investment of the project is expected to be about 183million euros, The funds are settled through the company's own funds and self raised funds; At the same time, the board of directors of the company authorizes the management to handle relevant investment matters and sign relevant resolutions, agreements and other legal documents.

11-13

Nanyang shares:Beijing Tianrongxin Network Security Technology Co., Ltd., a wholly-owned subsidiary of Nanyang Tianrongxin Technology Group Co., Ltd., and a wholly-owned subsidiary of Beijing Tianrongxin Technology Co., Ltd., plans to invest 10million yuan in Ningbo, Zhejiang Province to establish a wholly-owned subsidiary, Ningbo Tianrongxin Network Security Technology Co., Ltd.

11-14

Ganfeng lithium:Jiangxi Ganfeng Lithium Industry Co., Ltd. agreed to increase the capital of its wholly-owned subsidiary Ganfeng international trade (Shanghai) Co., Ltd. by 200 million yuan with its own funds. The original registered capital of Shanghai Ganfeng was 500 million yuan, and the registered capital after the capital increase was 70 million yuan. The company holds 100% of its equity.

Ganfeng lithium:Jiangxi Ganfeng lithium Co., Ltd. agreed that Shanghai Ganfeng, a wholly-owned subsidiary of the company, would increase the capital of Sonora by exercising the call option with its own funds at the price of £ 0.2959 per share, and the transaction amount would not exceed £ 23million. Before the completion of this transaction, Shanghai Ganfeng held 22.5% equity of Sonora; After the completion of this transaction, Shanghai Ganfeng holds no more than 50% equity of Sonora.

*St Kelu:Shenzhen chedian Network Co., Ltd., the holding subsidiary of Shenzhen Kelu Electronic Technology Co., Ltd., signed the strategic cooperation framework agreement with Shenzhen shunyitong Information Technology Co., Ltd., the holding subsidiary of Shenzhen Jieshun Technology Industry Co., Ltd., on November 12, 2020, to seize the key opportunities for the development of the new energy vehicle industry, relying on the strong offline resource advantages and comprehensive comprehensive capabilities of both sides, With the smart parking industry and new energy vehicle charging services as the core, build multiple online and offline application scenarios, and provide integrated parking, travel, charging and other intelligent management and operation services.

GP:Guangzhou Penghui Energy Technology Co., Ltd. held the fourth meeting of the Fourth Board of directors on November 13, 2020, deliberated and passed the proposal on carrying out foreign exchange hedging business, and agreed that the company and its subsidiaries should carry out foreign exchange hedging business from the date of deliberation and approval by the board of directors, with an annual amount of not more than 250 million yuan (or equivalent foreign currency).

New world:Shenzhen xinzhoubang Technology Co., Ltd. plans to purchase 74.24% of the equity of Jiangsu jiujiujiu Technology Co., Ltd. held by Yan'an Bikang Pharmaceutical Co., Ltd. by paying cash.

Huichuan Technology:On November 12, 2020, the company held the 31st meeting of the Fourth Board of directors, deliberated and passed the proposal on adjusting the commodity futures hedging business of subsidiaries, and agreed that the company should make the following adjustments to the commodity futures hedging business: ① add Suzhou Huichuan, united power, the main body for the implementation of commodity futures hedging business; ② New trading varieties of aluminum and silver; ③ Increase the daily balance of commodity futures hedging business from no more than 60million yuan to no more than 300million yuan. After the adjustment, the implementers of commodity futures hedging business were changed to best (including its subsidiaries), Suzhou Huichuan and united power, the trading varieties were changed to copper, polyvinyl chloride, aluminum and silver, and the daily balance was changed to no more than 300million yuan.

Huichuan Technology:The government subsidies of Shenzhen Huichuan Technology Co., Ltd. and its subsidiaries are mainly VAT levied and refunded, and a few are government subsidies obtained by declaring in the form of projects; The preceding paragraph involves many corporate entities, including the parent company and some subsidiaries. From September 1, 2020 to October 31, 2020, the company and its subsidiaries received various government subsidies totaling 68747230.63 yuan, which are related to income, accounting for 7.22% of the company's audited net profit attributable to shareholders of Listed Companies in 2019. Among the government subsidies obtained, the government subsidy fund for VAT collection and refund is 61248113.72 yuan, and the government subsidy fund for scientific research projects and other government subsidies is 7499116.91 yuan.

8.2 issuance of stocks and bonds, credit guarantee, idle fund management

11-09

Tianneng heavy industry:Qingdao Tianneng Heavy Industry Co., Ltd. plans to issue no more than 64462065 shares (including this number) to Zhuhai port group, a specific object, and no more than 30% of the company's total share capital of 391866660 shares (117559998 shares) before this issue. The total amount of funds raised from this issuance of shares to specific objects does not exceed 1001095869.450 yuan (including this amount), which will be used to repay the company's debts after deducting the issuance expenses.

11-10

Current shares:Anhui Yingliu electromechanical Co., Ltd. will privately issue 54207745 restricted circulating shares on November 16, 2020.

Neo state: Shenzhen xinzhoubang Technology Co., Ltd. privately issued 32758620 shares at an issue price of 34.80 yuan / share. The new shares are expected to be listed and circulated on November 12, 2020. After the completion of this non-public offering, the total share capital of the company increased from 378034293 shares to 410792913 shares.

New world:Shenzhen new Zeon Technology Co., Ltd. held the seventh meeting of the Fifth Board of directors on November 9, 2020, and deliberated and passed the proposal on applying for loans from banks with their own assets as collateral. It agreed that the company would apply for a loan of no more than 400million yuan from Shenzhen Branch of the export Import Bank of China with its own assets as collateral according to business development and daily business needs, with a term of no more than 3 years, The mortgaged assets are the land and real estate of Shenzhen new Zhoubang science and technology building, which are used to supplement the working capital of the company.

Goldwind Technology:Goldwind Australia Pty Ltd, a wholly-owned subsidiary of Goldwind International Holdings (Hong Kong) Co., Ltd., a wholly-owned subsidiary of Xinjiang Goldwind Technology Co., Ltd., signed a unit supply and installation agreement with juwi renewable energy Pty Ltd, for which Goldwind Australia will provide units and installation services. Goldwind technology signed a general guarantee agreement with juwi to provide parent company guarantee for Goldwind Australia's performance obligations under the above unit supply and installation agreement. The guarantee amount is equivalent to about 84005700 yuan. The guarantee period is from the date of signing the guarantee contract to the time when Goldwind Australia completes its obligations under the unit supply and installation agreement.

Goldwind Technology:On November 9, 2020, the 13th meeting of the seventh board of directors of Xinjiang Goldwind Technology Co., Ltd. deliberated and passed the proposal on the equity transfer of the U.S. rattlesnake project and the guarantee provided by Goldwind technology, which agreed that Goldwind technology would provide joint and several liability guarantee for the performance and liquidated damages liability of the wholly-owned company rattlesnake power holding, LLC under the equity transfer agreement for the transfer of the U.S. rattlesnake project, The guarantee amount shall not exceed 70million US dollars.

11-11

Hanrui cobalt:Nanjing Hanrui cobalt Industry Co., Ltd. provides joint and several liability guarantee for the wholly-owned subsidiary Nanjing Hanrui cobalt industry (Hong Kong) Co., Ltd. to apply for a loan from Shanghai Commercial savings bank, with a guarantee amount of US $5.1 million and a guarantee period of 10 months.

Yiwei lithium energy:Hubei Yiwei Power Co., Ltd., a subsidiary of Huizhou Yiwei lithium energy Co., Ltd., plans to apply to Wuhan Branch of Ping An Bank Co., Ltd. for a comprehensive credit line of no more than 300 million yuan, with a credit term of one year. The company plans to provide joint and several liability guarantee for the above credit matters.

11-12

Zhenjiang shares:Jiangsu Zhenjiang New Energy Equipment Co., Ltd. held the 27th meeting of the second board of directors on October 29, 2020 to consider and adopt the proposal on providing loans to the holding subsidiary. The company will provide a total loan of no more than 150million yuan to the holding subsidiary Shanghe (Shanghai) offshore engineering equipment Co., Ltd. and sign the loan agreement, with a loan term of no more than 24 months, The loan interest rate refers to the bank loan interest rate of the same period.

11-13

Aixu shares:Shanghai aixu new energy Co., Ltd. plans to use part of the idle raised funds of 400000000 yuan to temporarily supplement the working capital, and the service life shall not exceed 12 months from the date of approval by the board of directors.

Taiwan Nuclear Power:Taiwan Manuel Nuclear Power Equipment Co., Ltd. has undergone major asset restructuring and issued shares to purchase assets and raise supporting funds. The shareholders applying for the lifting of share restrictions this time are su Sisi, Liu Yuan, Wei Hailong and Shen Junxi, with a number of 40000000 shares, accounting for 4.61% of the total share capital of the company. The listing and circulation date is November 16, 2020.

11-14

GP:Guangzhou Penghui Energy Technology Co., Ltd. was approved to issue 8900000 convertible bonds to unspecified objects, each with a face value of 100 yuan. The total amount of convertible bonds issued was 890000000 yuan. After deducting 19928000 yuan of sponsorship and underwriting fees (including tax), it actually received 870072000 yuan of convertible bond raised funds, and all the funds were remitted to the designated account of the company on October 26, 2020. In the process of this offering, the company shall pay a total of 22649078.98 yuan (including tax), including recommendation and underwriting fees, audit and verification fees, attorney fees, credit rating fees, information disclosure and other issuance fees for this offering, of which the issuance fee excluding tax is 21387861.97 yuan, and the actual net amount of raised funds after deducting the issuance fee excluding tax is 868612138.03 yuan.

Incheon Technology:On November 12, 2020, the company held the 31st meeting of the Fourth Board of directors and passed the proposal on using idle self owned funds to purchase bank financial products, agreeing that the company and its holding subsidiaries use temporarily idle self owned funds to purchase financial products, with a limit of daily financial balance of no more than RMB 5billion and a period of five years. This limit still needs to be considered by the general meeting of shareholders. Before the above limit is considered by the general meeting of shareholders, the company purchases financial products within the authority of the board of directors, that is, to purchase financial products within the range of daily financial balance of no more than RMB 800million (including this amount, the same below). This limit is effective for one year from January 17, 2021. After the approval of the general meeting of shareholders, the company will use idle self owned funds with a daily wealth management balance of no more than RMB 5billion to purchase wealth management products.

8.3Increase or decrease of shareholders, employee stock ownership, equity repurchase

11-09

Mingyang intelligent:Mingyang Smart Energy Group Co., Ltd. issued a suggestive announcement on the change of shareholders' equity holding more than 5%. During the period from April 30, 2020 to November 5, 2020, Guangzhou HuiFu Kaile investment partnership (limited partnership), the subject of this equity change, reduced a total of 63615728 shares of the company, of which 27610281 shares were reduced through centralized bidding and 36005447 shares were reduced through block trading. This equity change will not affect the control of the actual controllers of the company, Mr. Zhang Chuanwei, Ms. Wu Ling and Mr. Zhang Rui. After this equity change, HuiFu Kaile held 101830609 shares of the company, accounting for 6.97% of the company's current total share capital (i.e. 1460751982 shares), and is still more than 5% of the company's non largest shareholder.

Tianneng heavy industry:Qingdao Tianneng Heavy Industry Co., Ltd. received the share transfer agreement signed by the controlling shareholder Mr. Zheng Xu and Zhuhai port group and the share transfer agreement signed by the shareholder Mr. Zhang Shiqi and Zhuhai Port Group on November 6, 2020. Mr. Zheng Xu plans to transfer 50203125 shares (accounting for 12.81% of the total share capital of the listed company) of his shares in the listed company to Zhuhaigang group in two times, and give up his voting rights to hold the shares of the listed company after the completion of the first share transfer; Mr. zhangshiqi plans to transfer his shares in the listed company (accounting for 5.56% of the total share capital of the listed company) to Zhuhai port group, and gives up his voting rights to hold the shares of the listed company after the completion of the first share transfer. Zhuhai Port Group will therefore become the controlling shareholder of the company, and the actual controller of the company will be changed to Zhuhai SASAC.

11-10

Longji shares:Mr. lizhenguo, the controlling shareholder of Longji Green Energy Technology Co., Ltd., handled the early release of the pledge of 13000000 non tradable shares pledged to BOC International Securities Co., Ltd. on November 6, 2020. After the release of the pledge, the cumulative number of Pledged Shares of the company was 142596000, accounting for 26.19% of its holdings.

University of science and Technology Intelligence:Some shares of the company held by Mr. Huang Mingsong, the controlling shareholder and actual controller of HKUST Intelligent Technology Co., Ltd., were released from pledge and supplementary pledge. Among them, 8000000 shares were released from pledge, accounting for 4.18% of its shares and 1.11% of the total share capital of the company. The deadline is November 5, 2020; The supplementary pledge is 2398810 shares, accounting for 1.25% of its shares and 0.33% of the total share capital of the company. The starting date is November 6, 2020.

Heshun Electric:Mr. Yao Jianhua, the controlling shareholder and actual controller of Suzhou Industrial Park Heshun Electric Co., Ltd., plans to reduce his holdings of no more than 5077692 shares of the company (accounting for 2% of the total share capital of the company) in the form of centralized bidding within six months after 15 trading days from the date of this announcement; Mr. Yao Jianhua promised that the total number of shares reduced through the centralized bidding transaction of the stock exchange within 90 consecutive natural days would not exceed 1% of the total number of shares of the company; Mr. Shen Xin, a shareholder holding more than 5% of the company's shares, plans to reduce the company's shares by centralized bidding within six months after 15 trading days from the date of this announcement by no more than 4000000 shares (accounting for 1.5755% of the company's total share capital); Mr. Du Jie, the person acting in concert, plans to reduce the shares of the company by centralized bidding within six months after 15 trading days from the date of this announcement by no more than 500000 shares (accounting for 0.1969% of the total share capital of the company). Mr. Shen Xin and Mr. Du Jie jointly promised that the total number of consolidated shares reduced through centralized bidding trading on the stock exchange within 90 consecutive natural days would not exceed 1% of the total number of shares of the company.

Tongwei shares:Tongwei Group Co., Ltd. holds 46.61% of the shares of Tongwei Co., Ltd. and is the controlling shareholder of the company. On November 9, 2020, Tongwei group released the pledge of 22000000 shares pledged to Chengdu Branch of Industrial Bank Co., Ltd. As of the disclosure date of the announcement, Tongwei group has pledged 788107151 shares, accounting for 18.38% of the total share capital of the company and 39.44% of the total shares of the company held by it.

Shenghui Technology:Shenghui Intelligent Technology Co., Ltd. recently received a notice from Mr. jifaqing, the controlling shareholder and actual controller of the company. Based on his own capital needs, Mr. jifaqing plans to reduce his holdings of no more than 8million shares of the company through the trading system of Shenzhen Stock Exchange (including but not limited to block trading and call auction) (that is, no more than 1.6022% of the current total share capital of the company). After the maximum implementation of this stock exchange, the actual controller of the company is still Mr. jifaqing, which will not lead to the change of the company's control.

Jingao Technology:On November 9, 2020, Jingao Solar Energy Technology Co., Ltd. received a notice from Shenzhen Huajian Yingfu investment enterprise (limited partnership), a shareholder holding more than 5% of the company's shares, and some shares of the company held by Huajian Yingfu were released from pledge. The pledge of 4700000 shares was released, accounting for 3.32% of its shares and 0.29% of the total share capital of the company.

GP:On November 9, 2020, the company received the notification letter from the controlling shareholder, Mr. Xia Xinde. On November 6, 2020, Mr. Xia Xinde reduced his holdings of 2880000 Penghui convertible bonds through block trading through the Shenzhen stock exchange system, accounting for 32.3596% of the total issuance.

11-11

Hongfa shares:Lianfa Group Co., Ltd. holds 71934814 shares of Hongfa Technology Co., Ltd., accounting for 9.66% of the total share capital of the company, all of which are tradable shares with unlimited sales conditions. MediaTek group plans to reduce its holdings of Hongfa shares by centralized bidding, with a total of no more than 7440000 shares, that is, no more than 1% of the total shares of the company.

Tianqi lithium: on November 10, Tianqi lithium Co., Ltd. received the short form equity change report of Tianqi lithium Co., Ltd. issued by the controlling shareholder Tianqi industry (Group) Co., Ltd. From March 12, 2014 to the signing date of this equity change report, 64186919 shares of the company's shares were reduced through centralized bidding and block trading in Shenzhen Stock Exchange, accounting for 4.35% of the current total share capital of Tianqi lithium.

11-12

Shi dashenghua:Shandong Shida Shenghua Chemical Group Co., Ltd.) plans to plan an employee stock ownership plan on September 12, 2020. However, due to the differences in subjective and objective conditions such as the income level and risk tolerance of many employees of the company, it is difficult to reach an agreement on the source of funds of the employee stock ownership plan. After careful study, the company decided to terminate the planning of the employee stock ownership plan and start it when the conditions are ripe.

Enjie shares:Yuxi Heyi Investment Co., Ltd., a shareholder holding more than 5% of Yunnan Enjie new materials Co., Ltd., lifted the pledge of some 16274000 shares of the company held by it on November 10, 2020. The Pledged Shares released this time accounted for 13.62% of its shares and 1.85% of the total share capital of the company.

Taiwan Nuclear Power:During the period from May 26, 2020 to November 9, 2020, Taiwan Strait group reduced its holdings of 111232882 shares through judicial auction, accounting for 12.83% of the total share capital of the company. After the equity changes are completed, the number of shares held by Taiwan Strait group in the company is 262436862, accounting for 30.27% of the total share capital of the company.

11-13

Tongwei shares:Tongwei Group Co., Ltd. holds 46.61% of the shares of Tongwei Co., Ltd. and is the controlling shareholder of the company. Tongwei Group pledged 16000000 shares on November 11, 2020, accounting for 0.80% of its shareholding and 0.37% of the total share capital of the company. As of the disclosure date of the announcement, Tongwei group has pledged 804107151 shares, accounting for 18.75% of the total share capital of the company and 40.24% of the total shares of the company held by it.

Ganfeng lithium:Mr. Li Liangbin is the largest shareholder of Jiangxi Ganfeng lithium Co., Ltd. and currently holds 269770452 shares of the company, accounting for 20.24% of the total share capital of the company. Mr. Li Liangbin plans to apply to the Shenzhen Branch of China Securities Depository and Clearing Corporation for non trading transfer of securities, and transfer no more than 1.6 million shares he holds to the "Guojin securities Xinjin No. 9 single asset management plan", which will be managed by the manager Guojin Securities Co., Ltd. within the authority specified in relevant laws, regulations and contracts as entrusted assets. This action will not change the number of shares of the company held by Mr. Li Liangbin.

Star source material:Mr. Chen Xiufeng, the controlling shareholder and actual controller of Shenzhen Xingyuan Material Technology Co., Ltd., handled the pledge release of some shares of the company he held. The number of pledged shares released this time is 12527325, accounting for 15.36% of its shares and 2.79% of the total share capital of the company. The release date is November 11, 2020.

Longji shares:In view of the fact that eight of the incentive objects in the second phase of the company's restricted stock incentive plan have resigned and the relevant repurchase materials have been provided, the company agrees to repurchase and cancel 58450 shares of restricted shares granted to the above incentive objects but not unlocked.

Tianneng heavy industry:Qingdao Tianneng Heavy Industry Co., Ltd. held the 40th meeting of the third board of directors on October 29, 2020. In view of the fact that the exercise conditions for the first exercise period of the reserved stock options in the 2018 stock option incentive plan have been met, it was agreed that the company should handle the matters related to the exercise of the first exercise period of the reserved stock options in accordance with the relevant provisions of the incentive plan. A total of 23 incentive objects met the exercise conditions this time, and the number of stock options that can apply for exercise is 2214675, accounting for 0.57% of the total share capital of the company. This exercise adopts the independent exercise mode.

11-14

Tuorixinneng:Shenzhen tuori New Energy Technology Co., Ltd. recently received a letter from the controlling shareholder Shenzhen AoXin Investment Development Co., Ltd. and learned that it would release the pledge of some of its shares in the company and then pledge. The pledge amount is 35 million shares, accounting for 8.92% of its shares and 2.83% of the total share capital of the company. The pledge start date is November 11, 2020.

GCL integration:GCL Integrated Technology Co., Ltd. received a letter from GCL Group Co., Ltd., the controlling shareholder of the company, and Yingkou Qiyin Investment Management Co., Ltd., who acted in concert, on November 13, 2020, and learned that GCL group and Yingkou Qiyin jointly reduced 82939700 shares of the company through block trading through the trading system of Shenzhen Stock Exchange on November 11, 2020 and November 13, 2020, accounting for 1.63% of the total share capital of the company. According to relevant laws and regulations, the transferee of this block transaction will not transfer its transferred shares within six months after the transfer.

GCL integration:GCL Group Co., Ltd., the controlling shareholder of the company, holds 497177945 shares of the company, accounting for 9.78% of the total share capital of the company. Due to operation and capital related arrangements, it is proposed to reduce GCL integrated shares by centralized bidding within 6 months after 15 trading days from the date of the announcement of this reduction plan, accounting for 0.98% of the total share capital of the company.

8.4 personnel changes at the top of the company

11-09

Jingao Technology:On November 7, 2020, Jingao Solar Energy Technology Co., Ltd. learned from Jinglong Industrial Group Co., Ltd. that it received a notice from Pingdu municipal supervisory committee that Mr. Jin Baofang, the actual controller, chairman and general manager of the company, was filed for investigation and detention by Pingdu municipal supervisory committee in accordance with the supervision law of the people's Republic of China.

Pioneer Intelligence: the board of directors of Wuxi pioneer Intelligent Equipment Co., Ltd. agreed to appoint Mr. Zhou Jianfeng as the deputy general manager and Secretary of the board of directors of the company on November 9, 2020. The term of office starts from the date of deliberation and approval of this board of directors to the expiration of the term of office of the third board of directors. Mr. Wang Yanqing, chairman of the company, will no longer perform the duties of secretary of the board of directors.

11-13

Jiuli special material:The first meeting of the 6th board of directors of Zhejiang Jiuli special material technology Co., Ltd. was held in the company's conference room on November 12, 2020 by means of on-site voting combined with communication. The meeting elected Mr. Li Zhengzhou as the chairman of the sixth board of directors of the company; Appoint Mr. Li Zhengzhou as the general manager of the company; Appoint Mr. wangchangcheng as the executive deputy general manager of the company; Appoint Mr. Xu Amin, Mr. Zhang Jianxin and Ms. Zhou Yubin as deputy general managers of the company; Appoint Mr. Su Cheng as the chief engineer of the company; Appoint Ms. Yang Peifen as the financial director of the company; Appoint Mr. shouhaotian as the Secretary of the board of directors and MS. yaohuiying as the representative of the company's securities affairs; Appoint Ms. zhuweilin as the head of the company's internal audit department. The term of office of the above-mentioned senior managers is three years, calculated from the date of adoption of this board meeting to the date of expiration of this board of directors.

Jiuli special material:Zhejiang Jiuli special material technology Co., Ltd. recently held a staff representative meeting in the company's conference room. After careful consideration by the staff representatives present, it was agreed to elect Mr. Shen Xiaogang as the staff representative supervisor of the sixth board of supervisors of the company, which will form the sixth board of supervisors of the company together with the two shareholder representative supervisors elected by the third extraordinary general meeting of the company in 2020. The term of office of the sixth board of supervisors is the same as that of the sixth board of supervisors.

Jiuli special material:According to the resolution of the third extraordinary general meeting of shareholders of Zhejiang Jiuli special material technology Co., Ltd. in 2020, Mr. Zhou Zhijiang, Mr. Li Zhengzhou, Mr. Zhang yuxu, Mr. Xu Amin, Ms. Yang Peifen and Mr. Cai Liming were elected as non independent directors of the sixth board of directors of the company; Elect Mr. Zheng Wanqing, Ms. Miao Lanjuan and Mr. Sun Hanhong as independent directors of the sixth board of directors of the company; Mr. Shi Quanbing and Mr. Shen Yufeng were elected as non employee representative supervisors of the sixth board of supervisors of the company, and together with the employee representative supervisors, they formed the sixth board of supervisors of the company. The term of office of the above-mentioned personnel is three years from the date of deliberation and approval of this general meeting of shareholders.

nine

Risk statement

The sales volume of new energy vehicles is less than expected;